Lodging Analytics Research & Consulting (LARC)’s 2Q-2022 Hotel Industry Outlook and Market Intelligence Reports

Currently, the U.S. economy and hotel industry are facing a variety of uncertainties. We attempt to incorporate all of these risks into our national and market level outlooks. However, each of these uncertainties can have varying levels of implications: which we discuss below.

Risks From New Covid-19 Variants - While the effects of both the Delta and Omicron variants were short-lived, there is no doubt that both variants disrupted the travel recovery during the second half of 2021 and early 2022. However, it should be noted that the impact from Omicron, while no less severe, was far briefer than the impact from Delta. While there remains risk of new variants emerging, we expect any such impact to be less significant than the previous, as the U.S. attempts to move beyond the pandemic. The one exception being a vaccine resilient strain of the virus. We do not assume any new variants emerge in our outlook.

Elevated Inflation – CPI rose over 8% in March and Aprilthe highest rate of increase since 1981. We believe inflation has been fueled by several factors, including but not limited to elevated home prices, high auto prices, supply chain disruptions, and the rising cost of oil and gas. We believe all of these issues are transitory in nature and will begin to ease in the near-term. By 3Q-2022, Moody’s Analytics expects inflation to be down to 3.3% and to be under 3% thereafter.

- Housing Costs (31% of inflation) - The Federal Reserve has already raised the fed funds rate 75 bps year-to-date and has hinted that additional 50-bp increases are on the table to help curb inflation. The April 2022 average 30-year fixed-rate mortgage from Freddie Mac was 4.98%, which is 190 bps above year-end levels. While home prices may not have materially declined yet, that is due in part to the lag between a property going under contract at newer higher rates and the closing of the transaction. We expect higher mortgage rates to undoubtedly have a material effect on the housing market. As the housing market cools, it will have an outsized impact on inflation.

- Auto Costs (9% of inflation) – Since the early days of the pandemic, auto costs have been elevated due to a global computer chip shortage. The dearth causes a reduction in the production of new automobiles which in turn created added demand for the available inventory of both new and used vehicles. In fact, U.S. auto production in 2021 was 35% below 2019 levels. Experts indicate that the computer chip shortage will ease throughout the year with hopes of being fully resolved by early 2023. Beginning in March production volumes began to increase on a yearover-year basis for the first time since 2019.

- Supply Chain Issues – It is estimated that supply chain disruption cost the global economy a full percentage point of growth in 2021. With lockdowns across China and the war in Ukraine, it is unknown exactly when these issues will ease, however, it is likely to in the not-too-distant future as both of those issues appear to be transitory in nature. Though, there is risk of the war in Ukraine persisting far longer.

- Russian Invasion of Ukraine – Russia is the 40th largest trade partner of the U.S. As such, the economic sanctions placed on Russia are unlikely to have a significant impact on the U.S. However, Russia produces 10% of the world’s oil and 17% of the world’s natural gas and is the largest provider to Europe for both. That has caused a spike in oil and gas prices that is being felt globally. The good news is that U.S. production has begun to ramp up, and Moody’s Analytics expects prices to peak this quarter.

Rising Interest Rates - As mentioned, the Federal Reserve has already raised the fed funds rate 75 bps year-todate and has hinted that additional 50-bp increases are on the table to help curb inflation. While the Fed has taken a very aggressive stance at attempting to curb inflation, the risk is that control of the situation is beyond the Fed at this time. There are concerns that the Fed was too late to act, preventing rising interest rates from having the effect on inflation that the Fed is hoping. Rising interest rates will undoubtedly slow economic growth, but if inflation moderates as we expect in the coming months, the Fed will be able to be less aggressive with interest rate hikes than the market currently fears. As such, the impact on economic growth could be more muted.

Risk of Recession - We do believe recession is possible, though unlikely, over the next twelve months. It will hinge on the moderation of inflation without the Fed needing to be overly aggressive with interest rates moving forward. Our assumption is that the U.S. does not slip into recession over the next twelve months. However, we would also highlight that if it does occur, it is likely to be extremely mild and brief and may not have much impact on hotel operating fundamentals. Afterall, 1Q-2022 Real GDP declined an estimated 1.4%, yet U.S. RevPAR was up 66.5%. It will, however, impact the pace of the recovery.

Despite these uncertainties, leisure travel has continued to be incredibly strong while corporate transient and group travel have been gradually accelerating. Perhaps what has been most impressive in recent months is the strength in the lodging industry’s ADR recovery. The broader U.S. industry has generated average daily rates in excess of 2019 levels consistently for almost a year despite limited demand levels.

However, we acknowledge that the corporate recovery will be dependent on the return to the office, but we expect that to continue to gain momentum gradually through 2022 and into 2023. Additionally, while group attendance may be lighter than historically, the number of events is recovering rapidly, helping generate a base level of demand that will further support pricing power.

Under that backdrop, the economic forecast from Moody’s Analytics which drives our models makes the following key national assumptions:

- The Fed will raise rates by another 50 bps in 2022.

- Elevated inflation is transitory, but labor supply constraints will be slow to ease.

- Moody’s Analytics forecasts U.S. GDP to increase 3.6% in 2Q-2022 and 2.8% in 2022.

We continue to expect there to be markets that materially exceed pre-pandemic levels and others that continue to be well behind those levels. While year-over-year growth may be strongest in some markets that have experienced the least amount of recovery to date, it is off a low base, and many of the markets that have already recovered will still drive the best returns relative to pre-pandemic levels. We generally believe leisure markets will remain strong, while international gateway markets will take the longest to fully recover to pre-pandemic levels. Sector participants will need accurate, transparent, and detailed data to decipher between winning and losing markets, especially if they wish to take advantage of market dislocations that may occur in the near-term.

We believe the best business decisions are based on the best information available at the time of making that decision. We take that approach with our forecasts, using the best available information to provide the most likely outcome. As such, we believe transparency surrounding forecasting is critical to the lodging industry, which is why we are transparent with our clients, not just on what our forecasts are, but how we arrived at them.

LARC’s industry-leading market intelligence referred to throughout this document will help all industry participants navigate the current environment and position themselves for success as the recovery progresses. Please contact us directly to learn more about our services and products and if there is any other way we may be able to better serve you.

LARC’s Industry Outlook

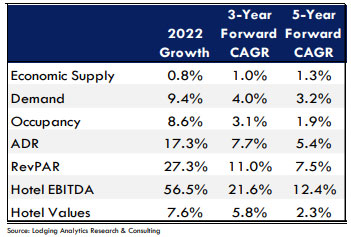

Currently, Lodging Analytics Research & Consulting (LARC) expects U.S. RevPAR to increase by 27.3% to $91.48 in 2022, which would put 2022 RevPAR 5% above 2019 levels. The recovery is driven by continued strength in ADR. LARC expects ADR to be up 17.3% this year to $146.19, which is 11% above 2019 levels. However, LARC has a more conservative view of the occupancy recovery. LARC expects occupancy to rise 8.6% in 2022 to 62.6% and expects occupancy to stabilize around 63% in 2023, well below 2019 levels.

LARC also anticipates U.S. Hotel EBITDA to grow by almost 60% in 2022 and hotel values to increase 8% in 2022. We believe values will recover to 2019 levels this year and Hotel EBITDA will do so by 2023.

LARC’s U.S. RevPAR model has an R-squared of 99.5% with a standard error of 5.1%, back-tested to 2000. LARC’s U.S. Cap Rate model has an R-squared of 98.4% with a standard error of 22 bps, back-tested to 2005.

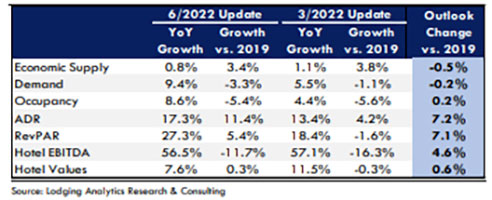

The tables below illustrate a summary of LARC’s current U.S. Hotel Industry Outlook in contrast to last quarter’s outlook. Ultimately, our 2022 outlook for supply and demand both modestly declined, while occupancy slightly improved. Our ADR outlook meaningfully improved driving an upward adjustment to our RevPAR outlook. However, our outlook for Hotel EBITDA and Values is minimally impacted.

March 2022 U.S. Hotel Industry Forecast Summary

2022 U.S. Hotel Industry Forecast: June 2022 Edition vs. March 2022 Edition

Market Outlooks

Below is a list of the best and worst performing markets based on our forecasts. Similar to our U.S. forecast, our market level forecasts are built entirely on multi-variable regression models with high historical accuracy (Rsquareds for each model seen on the next page).

More detail on our market outlooks can be found in LARC’s Market Intelligence Reports. Please contact us if you are interested in purchasing any of LARC’s offerings.

2022 (relative to 2019)

Top Markets for RevPAR Growth:

Tampa, Norfolk, Miami, Phoenix and Anaheim

Bottom Markets for RevPAR Growth:

San Francisco, Boston, New York, Washington, D.C. and Minneapolis

2022 (year-over-year)

Top Markets for RevPAR Growth:

San Francisco, Seattle, Washington, D.C., Minneapolis, and Honolulu

Bottom Markets for RevPAR Growth:

Norfolk, Miami, Detroit, Las Vegas, and Tampa

2019 - 2026 Outlook

Top Markets for RevPAR Growth:

Tampa, Miami, Norfolk, Anaheim, and Orlando

Bottom Markets for RevPAR Growth:

San Francisco, Boston, Washington, D.C., New York, and Atlanta

Top Markets for Value Change:

Tampa, Los Angeles, Denver, Phoenix, and Las Vegas

Bottom Markets for Value Change:

Chicago, San Francisco, New York, Washington D.C., and Detroit

Ryan Meliker

President

Lodging Analytics Research & Consulting, Inc