Consumer travel outlook better in the short-term amid increasing cost pressures, declining travel disruption and fewer COVID-19 concerns

Via STR’s Market Recovery Monitory through 12 November 2022, a pandemic-era high 52% of global hotel markets achieved real (inflation-adjusted) revenue per available room (RevPAR) above 2019 levels on a 28-day moving basis. In the U.S., 62% of markets exceeded their pre-pandemic comparable during the period.

In the face of mounting economic challenges, the war in Ukraine and soaring inflation in many parts of the world, these encouraging results highlight the continued resilient performance of the global hospitality industry.

Building on previous research conducted throughout the pandemic, STR canvassed opinion among consumers in November 2022 to better understand how macroeconomic factors and other issues, such as COVID-19, were influencing travel views and behaviors.

Short-term travel sentiment soars, long-term outlook lags

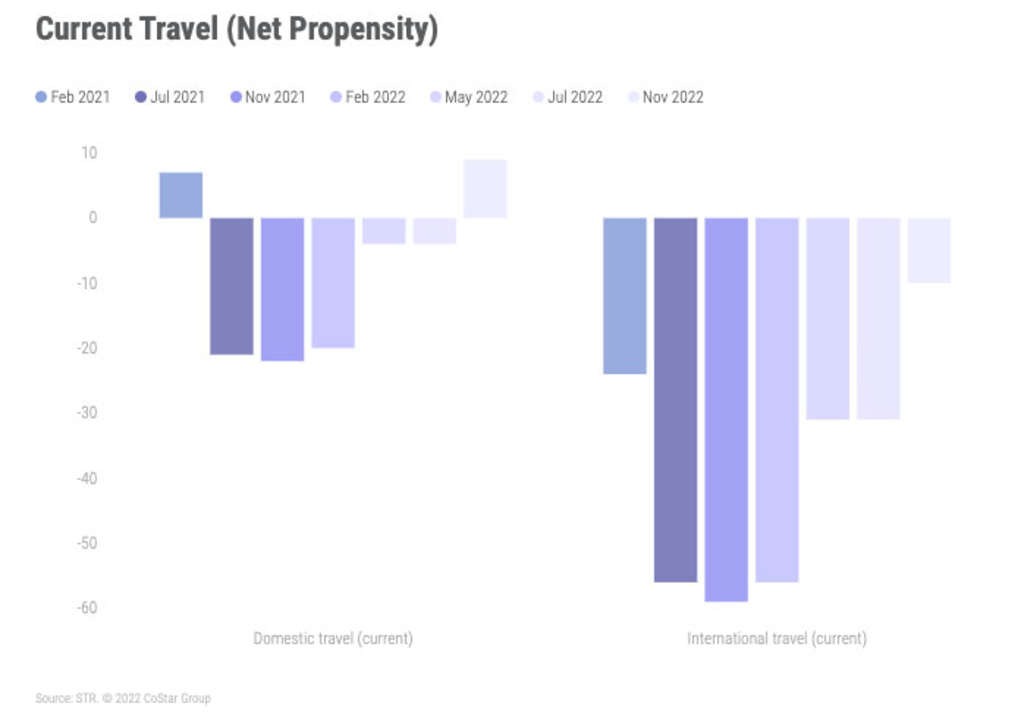

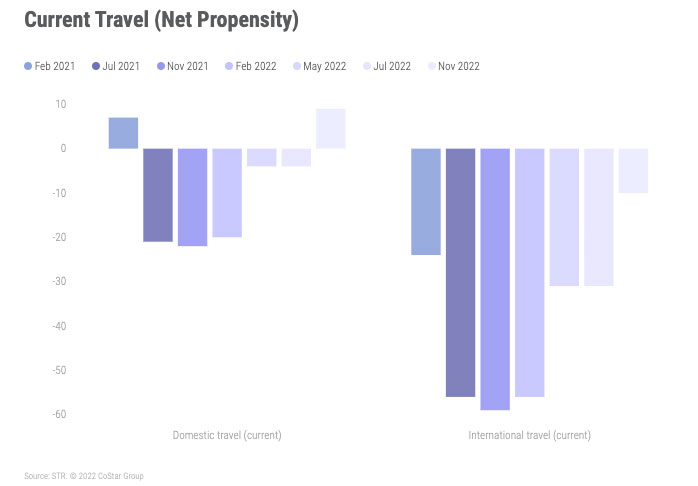

Sentiment toward current travel improved compared with previous STR surveys. Net propensity to travel, the difference between those who stated they were more or less likely to travel in the current situation, stood at +9% for domestic travel and -10% for international travel. These scores surpassed all previous results and, interestingly, were well above the last survey in July 2022.

The findings suggest that COVID-19 and travel disruption concerns, which were still stifling sentiment in July 2022, have waned in recent months. These factors combined with strong underlying demand have likely driven up the overall appeal of travel.

As many global economies report a slowdown in growth, the results also highlight that economic factors, at least for now, are playing a limited role in discouraging consumers from planning and undertaking trips.

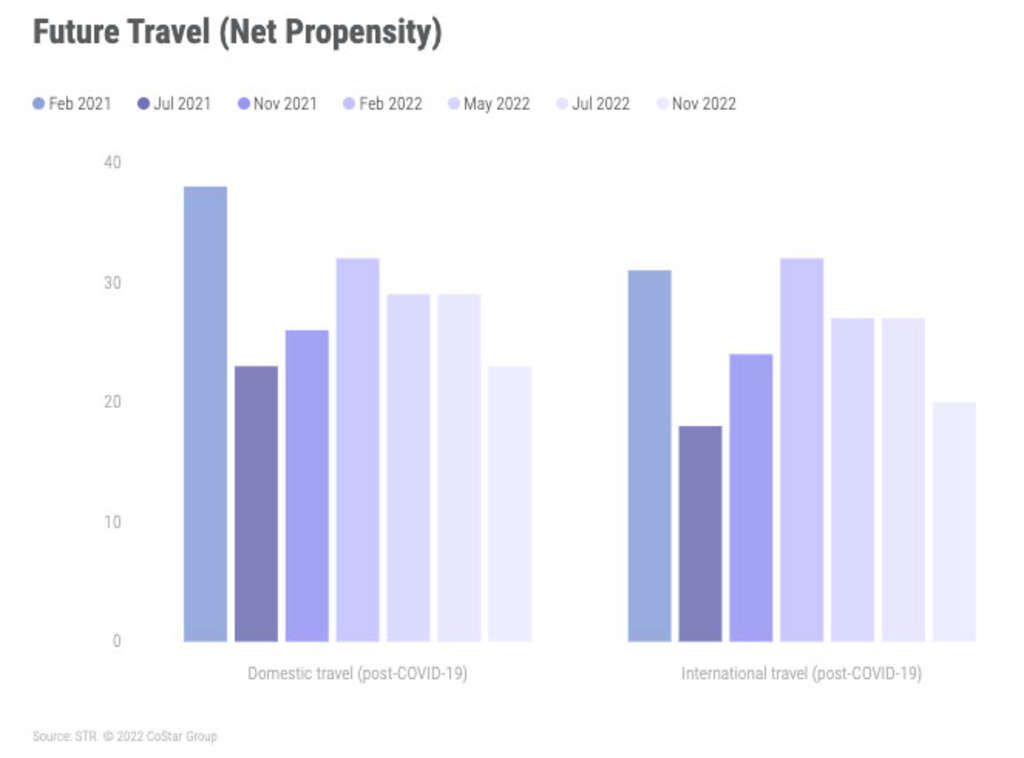

However, when looking to the future, there are signs of a slightly less optimistic outlook when comparing updated results with the most recent.

- November 2022, net propensity to travel in the future: +23% for domestic and +20% for international

- July 2022, net propensity to travel in the future: +29% for domestic and +27% for international

While the overall findings are positive, as they indicate that interest in travel will increase in the future, the latest results also suggest that travel aspirations for some have been downgraded recently, perhaps due to economic concerns.

Same but different concerns around travel

Consumers flagged modest concerns about hotel accommodation costs and were somewhat polarized about the impact of increased living costs and economic uncertainty on their travel plans. These findings were similar with July 2022, which is perhaps inconsistent as inflation and cost of living pressures have increased for most since the summer. However, it could be that consumers are prioritizing travel more currently, which may explain the positive short-term sentiment results.

Meanwhile, signaling a shift in view compared with July 2022, travel cancellations were considered less of an issue in November 2022 with 44% worried they might disrupt their next trip. That was down substantially from 59% earlier in the year. This is likely due to seasonality, as lower demand in the offseason places less strain on travel operators, but it may also be linked to capacity controls at airports and reduced staff shortages.

To gauge how demand may shift next year, respondents were probed about their travel intentions in 2023. Only 16% said that they were likely to travel less while the remainder (84%) stated that they would travel the same or more in 2023. These reassuring results reinforce earlier findings that the short-term outlook for travel looks healthy regardless of the challenging economic backdrop.

Financial barriers may be more costly on travel

The results discussed so far are encouraging for the industry as short-term travel sentiment improved and there was a similar view regarding future travel expenditure compared with July 2022.

However, assessing attitudes toward potential travel barriers compared with earlier in the year highlights that cost pressures have ratcheted up for consumers while travel disruption and COVID-19 concerns have lessened.

The three most significant barriers were financial factors:

- The cost of travel was considered the biggest issue, increasing from 61% to 64%.

- Concerns regarding personal financial situations increased the most, from 42% in July 2022 to 51%.

- The two remaining financial barriers—increasing household costs and uncertainty about the future economic situation—also increased, albeit only slightly compared with July 2022.

Balancing act: travel vs. finances

Collectively, the findings highlight growing sensitivity regarding costs and personal finances, which may stint future growth and could explain the dip in future sentiment revealed in this survey. However, evidence currently suggests that travel spend in the next 12 months is on par with the expectations of July 2022 when economic conditions in many countries were slightly better. This could mean that travel has become more important to some in recent months, despite increased economic headwinds. The extent to which personal financial situations are impacted or not over the coming weeks and months as economies adapt to global factors are likely to shape how travel spend is actualized.

About STR

STR provides premium data benchmarking, analytics and marketplace insights for the global hospitality industry. Founded in 1985, STR maintains a presence in 15 countries with a North American headquarters in Hendersonville, Tennessee, an international headquarters in London, and an Asia Pacific headquarters in Singapore. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), the leading provider of commercial real estate information, analytics and online marketplaces. For more information, please visit str.com and costargroup.com.