STR Weekly Insights: 21-27 January 2024

Countries (markets) mentioned:

- United States (Anaheim, Baltimore, Chicago, Colorado Area, Detroit, Las Vegas, Oahu, Orlando, San Francisco, Seattle)

- China, Germany, Japan, Spain (Madrid)

Highlights

- Strong U.S. RevPAR gains boosted by Las Vegas.

- U.S. group demand shows double-digit growth.

- Global RevPAR shows no sign of slowing even as COVID comparisons wane.

U.S. Performance

U.S. hotels saw big year-over-year (YoY) gains with revenue per available room (RevPAR) up 4.8%, driven entirely by a 5.1% increase in average daily rate (ADR). Occupancy sat at 56.2%, essentially matching the same week last year, down just 0.2 percentage points (ppts). As has been seen several times over the past couple months, the Las Vegas market with twice as many rooms as the next largest market and hosting large events had a significant impact on overall industry performance. Excluding Las Vegas, RevPAR grew a modest 1.4%, lifted by an ADR increase of 2.8%, which was offset by an occupancy decrease of 0.8 ppts.

Performance across the Top 25 Markets was strong with RevPAR up 10.8%, again boosted by Las Vegas. Excluding Las Vegas, the Top 25 Markets posted a RevPAR increase of 3.7%, with growth in both ADR (+2.5%) and occupancy (+0.7%).

There was a variety of high and low performers across the Top 25 Markets. Las Vegas led with RevPAR up 88.5% due to two large conventions: SHOT Show, which was a week later compared to last year and the World of Concrete. Chicago, the third largest market in terms of room supply, also posted a significant RevPAR increase, up 52.1% YoY, with advances in ADR (+21.2%) and occupancy (+11.5 ppts). Chicago hosted AHR (Air-Conditioning, Heating, Refrigeration) Expo at McCormick Place Convention Center. Other markets seeing double-digit RevPAR were Oahu, Orange County, Seattle, and Detroit. Eleven of the Top 25 Markets posted RevPAR gains above the industry average, while eight markets saw RevPAR go into arrears.

The rest of the country saw flat RevPAR (-0.4%), a combination of a falling occupancy (-1.5 ppts) partially offset by a 2.5% ADR increase. Baltimore, which hosted the NFL’s AFC Championship, and Colorado Area, which benefitted from a good ski week, were the two best performers outside the Top 25. Both saw RevPAR grow by more than 16%.

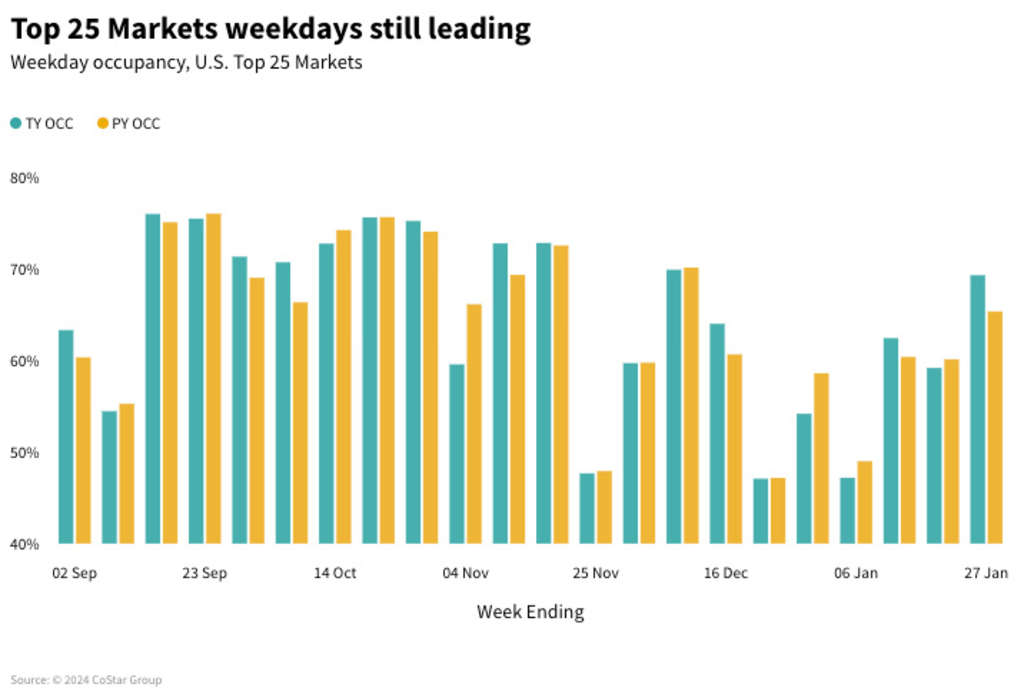

Top 25 Market weekday (Monday-Wednesday) performance continued to be the industry’s strongest performing segment, which was up 5.1%, driven by ADR (+2.6%) and occupancy (+1.6 ppts). Shoulder days (Sunday and Thursday) followed with RevPAR up 3.2% and weekends (Friday & Saturday) with a gain of 1.8%. The rest of the country saw weekday RevPAR increase 1.4% followed by shoulder days (-0.8%) and weekends (-2.4%).

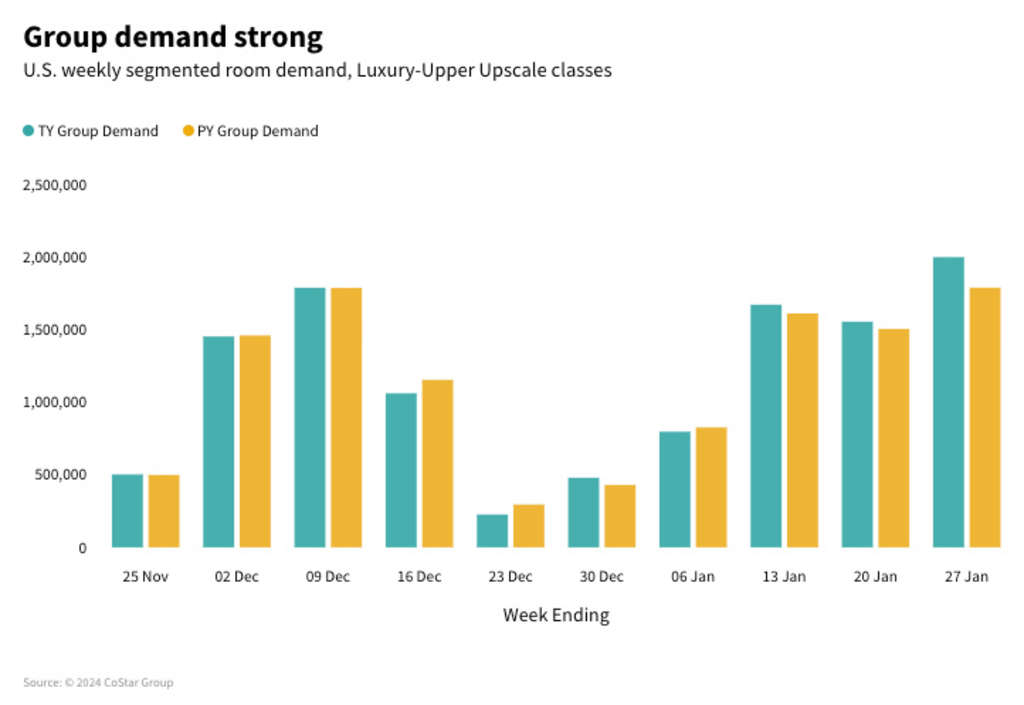

Group demand returned in full force, up 12% compared to the same week last year. Group demand has topped last year’s levels for the past three weeks, which is notable given that last January benefitted from a favorable post-Omicron surge in group demand. Year over year. Group ADR has also increased for the past three weeks. Markets posting group occupancy of more than four percentage points above last year were Las Vegas, Chicago, Oahu, Tampa, San Francisco, and Orlando.

Global hotel performance

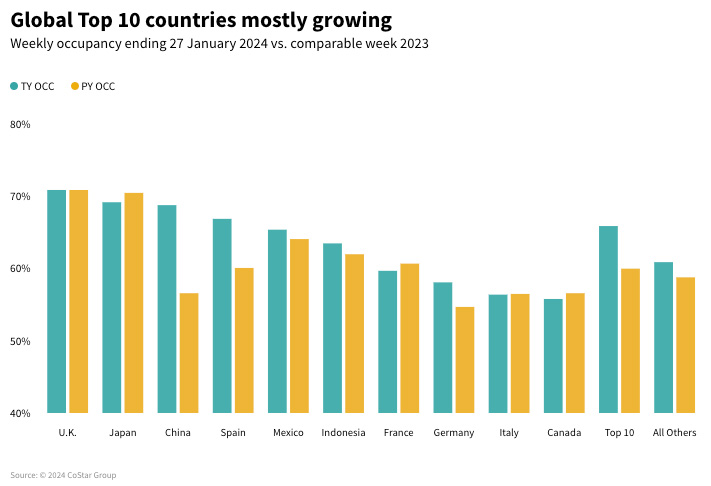

Outside of the U.S., the strongest occupancy performance within the top 10 countries, based on supply, was China (+12.2ppts). However, RevPAR declined 11.7%, a result of ADR decreasing 27.4% due to the shift in the Chinese New Year as the seven-day public holiday started last year on 22 January. This year, the holiday starts on 10 February.

Other high occupancy performing countries included Spain, up 6.7 ppts, which can be partially attributed to Madrid hosting the large annual international tourism Fair FITUR. Spain also had the second highest ADR gain (+16%), resulting in a 29.4% RevPAR increase.

Germany followed with the third highest occupancy gain, +3.4ppts and ADR up 12.4%, netting a RevPAR increase of 19.4%. Germany benefitted from a strong start to the year with several large fairs taking place across the country.

Japan also posted strong RevPAR fueled by ADR (+28.2%).

Overall, seven out of the top 10 countries posted RevPAR growth this week.

Looking ahead

U.S. hotel performance is expected to steadily improve over the next several weeks as business and group travel return, reaching a seasonal peak in mid-March. Year-over-year occupancy changes will be less volatile than last year, while ADR is expected to continue to increase. Leap Day on Thursday, 29 February will provide an extra revenue day for the month and report as such in weekly data. However, when reporting the month of February, data will be “grossed down” into a 28-day month to allow for a better like comparison. Super Bowl week is expected to boost performance in the host city, Las Vegas, and will likely impact U.S. performance. An early Easter (31 March) will impact March and Q1 year-over-year comparisons as last year Easter occurred on 9 April 2023.

Global markets, while expected to stabilize following last year’s strong performance as the impact of COVID comparisons wanes, continue to see strong performance. Holidays, in particular Chinese New Year, sporting events, concerts (Taylor Swift’s international tour), conferences/conventions, and the change of seasons will drive the ebb and flow of performance, and those changes should be more normal than what we have seen since March 2020.

*Analysis by Isaac Collazo, Chris Klauda, Will Anns

About STR

STR provides premium data benchmarking, analytics and marketplace insights for the global hospitality industry. Founded in 1985, STR maintains a presence in 15 countries with a North American headquarters in Hendersonville, Tennessee, an international headquarters in London, and an Asia Pacific headquarters in Singapore. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), the leading provider of commercial real estate information, analytics and online marketplaces. For more information, please visit str.com and costargroup.com.