Global Air Travel Capacity Set to Surpass Yearly Flight Figures in 2018 and 2019

Travel offered to both corporate and leisure clients combined is set to surpass the annual travel capacity in 2018 and 2019, that is according to FCM Consulting’s Q4-2023* Quarterly Global Trends Report, citing data from Cirium.

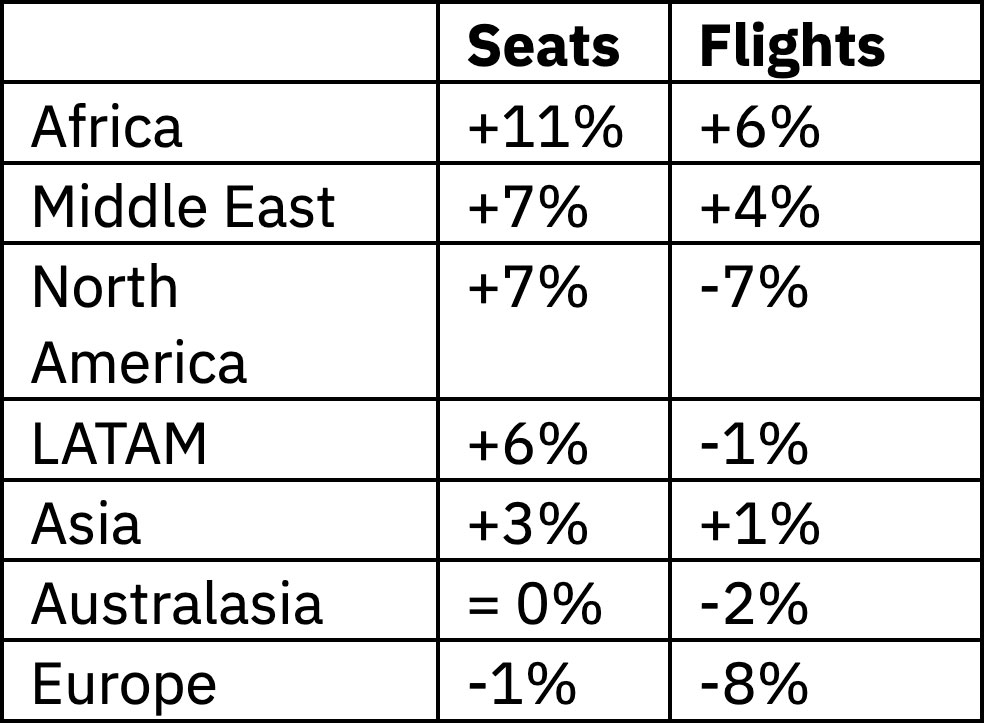

The report also highlighted a key trend that is set to continue for 2024 – more seats with fewer flights. H1-2024 is forecast to offer +97.9M (+3.5 per cent) more seats, and -2.1M (-5.6 per cent) fewer flights than H1-2019.

This is a result of fleet configuration changes and shifts in schedules to meet the demand. When carefully planned, this will be favourable to airline operating costs, staffing, airport slots and airport costs

said Sunny Sodhi, Managing Director of FCM Travel India.

Q4-2023 closed a milestone year, seeing corporate travel the busiest and least interrupted in over four years. Business travellers have become more confident than in previous years and are planning trips in 2024 to both grow their business and connect with clients and colleagues. Across the top global corporate airlines, we forecast that the seats offered in 2024 will be two per cent above 2019 and the number of flights offered will be down six per cent,

Sodhi said.

American Airlines, Delta Airlines, United Airlines, China Southern Airlines, China Eastern Airlines, LATAM Airlines Group, Qatar Airways, Cathay Pacific, Singapore Airlines, and Virgin Atlantic Airways are all forecast to be back over 100 per cent in terms of seats offered when compared to five years ago,

concluded Sodhi.

Mumbai to London saw a 25 per cent increase in economy class fares and a 24 per cent increase in economy class fares from Mumbai to Delhi. Business class fares from Mumbai to London increased by 13 per cent.

The top five domestic routes flown by business travellers in India are Chennai to Delhi, Delhi to Bangalore, Delhi to Mumbai, Mumbai to Bangalore and Mumbai to Delhi.

In terms of accommodation, the average room rates increased across all regions for 2023, when compared to 2022, with Asia seeing the highest rise globally of USD39.

Delhi commands the highest average room rate of USD$249, followed by Bangalore at USD 192 then Mumbai at USD$157. Chennai’s average room rate is USD$130 but it witnessed the highest increase of 35 per cent versus Q3-2023,

added Sodhi.

Despite the increased cost, all regions also saw a lift in occupancy levels year-on-year, with Mainland China – the last major nation to reopen its borders – leaping 34 per cent to have an occupancy rate of 65 per cent, Asia excluding China saw an increase of 17 per cent, and India saw an increase of 1.8 per cent to 70 per cent occupancy level in 2023.

*This FCM Consulting quarterly report draws on global data sourced from FCM Travel and Flight Centre Travel Group corporate booking data for travel from October to December 2023 (Q4-2023). The report uses Cirium aviation schedule data as of 18 January 2024. Airfare pricing variations exclude all taxes.

The hotel average room rate (ARR) quoted is the average booked rate using FCM Travel and Flight Centre Travel Group corporate booking data. Variations in rates booked reflect seasonality, supply, and demand, booking lead times and variations in exchange rates. Unless otherwise stated all fares and rates are reported in US dollars. STR hotel data and content were quoted as of January 2024 for the period ending December 2023.