STR Weekly Insights: 30 June – 6 July 2024

Countries/markets mentioned:

- United States: Denver, Houston, New Orleans, Oahu, Philadelphia, Seattle

- Global: France (Paris), Germany (Düsseldorf)

Highlights

- U.S. RevPAR fell as occupancy retreated and ADR stalled.

- Increased air travel and leisure outlook not translating into stronger U.S. RevPAR.

- Global occupancy tipped negative with moderating ADR growth.

- Euros continue to drive performance in Germany.

- Travelers still avoiding Paris as Olympics draw nearer.

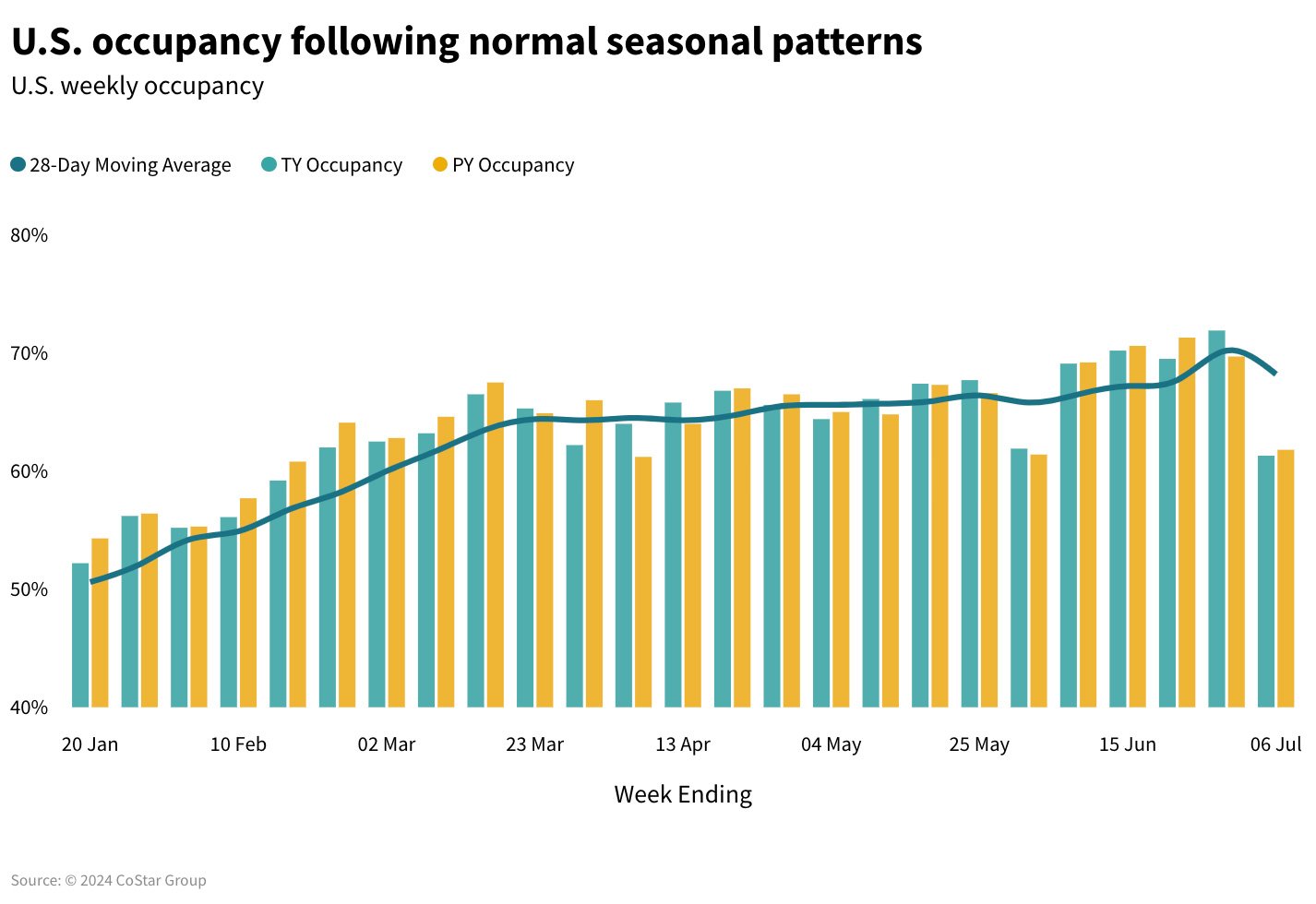

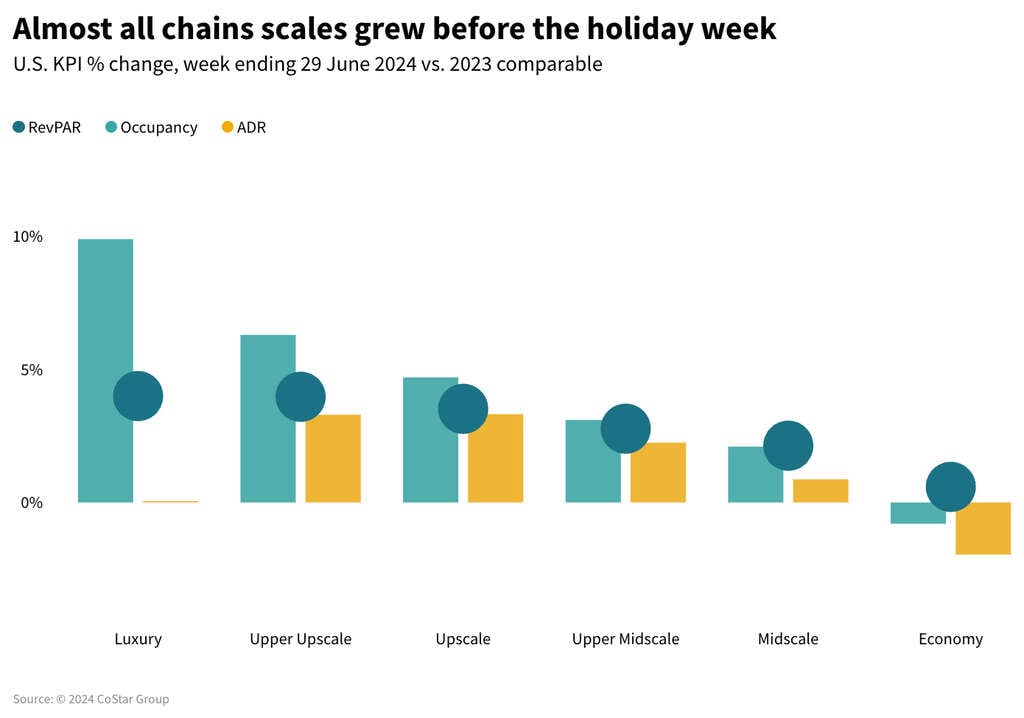

Seasonal dip in performance followed a healthy increase

Not surprising, weekly U.S. performance deviated from prior weeks due to the Fourth of July holiday. In the week ending 6 July 2024, revenue per available room (RevPAR) fell 0.4% after a 6.9% gain in the prior week. Significant RevPAR decreases (>-11%) were seen on Sunday and Monday, which were due to the shift in the holiday. Last year, the holiday fell on a Tuesday and resulted in tough comparisons early in the week. On the flip side, easy comparisons were seen on Wednesday through Friday as RevPAR increased more than 8% with the measure growing 19% on the actual holiday. Weekly occupancy fell 0.5 percentage points (ppts), and average daily rate (ADR) grew slightly (+0.5%).

There have only been four July 4th holidays on a Thursday since daily data performance benchmarking began in 2000—2002, 2013, 2019, 2024. This year’s room demand total was the second highest of the four behind 2019, but occupancy ranked third and was also behind 2019 (61.3% vs. 65.2%). ADR growth was the lowest of the four prior occurrences with all hotel classes showing flat to negative ADR comparisons except for Upper Upscale (+0.8%) and Economy (+0.2%).

As compared to the past 25 years, the week’s room demand was the seventh highest with the top mark achieved in 2021, however, occupancy ranked 20th. The highest occupancy for the holiday week was seen in 2015 (68.2%) when the 4th itself fell on a Saturday.

This year’s negative weekly RevPAR percentage change is not unheard of as it was down last year (-1.2%) and six other holiday weeks, excluding 2020, since 2000. However, this was the first time RevPAR was down as compared to the previous three when the 4th fell on a Thursday.

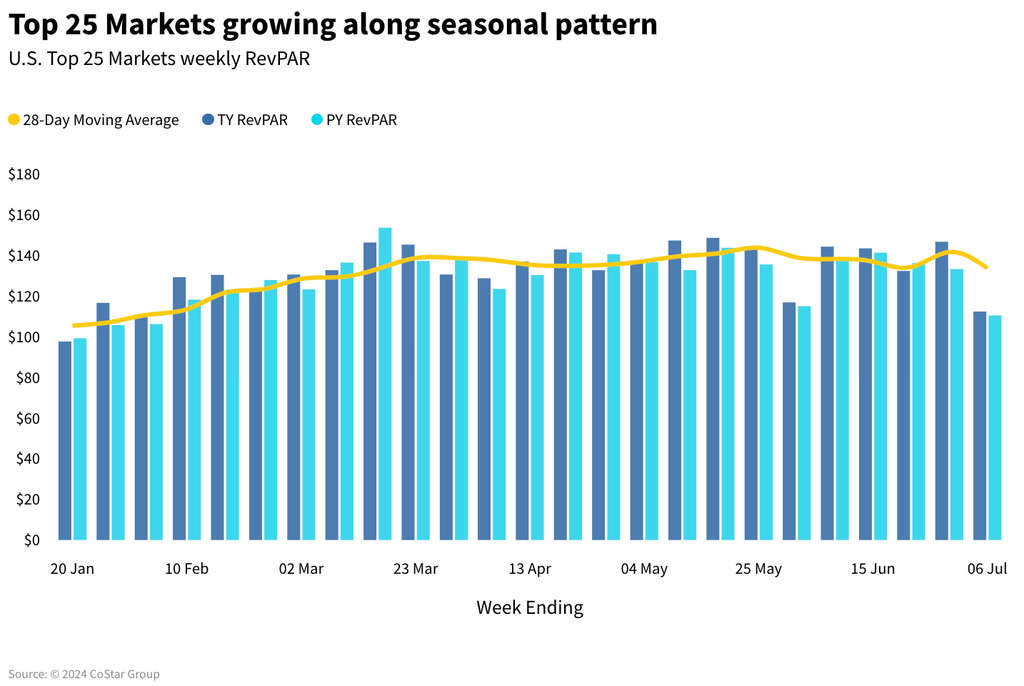

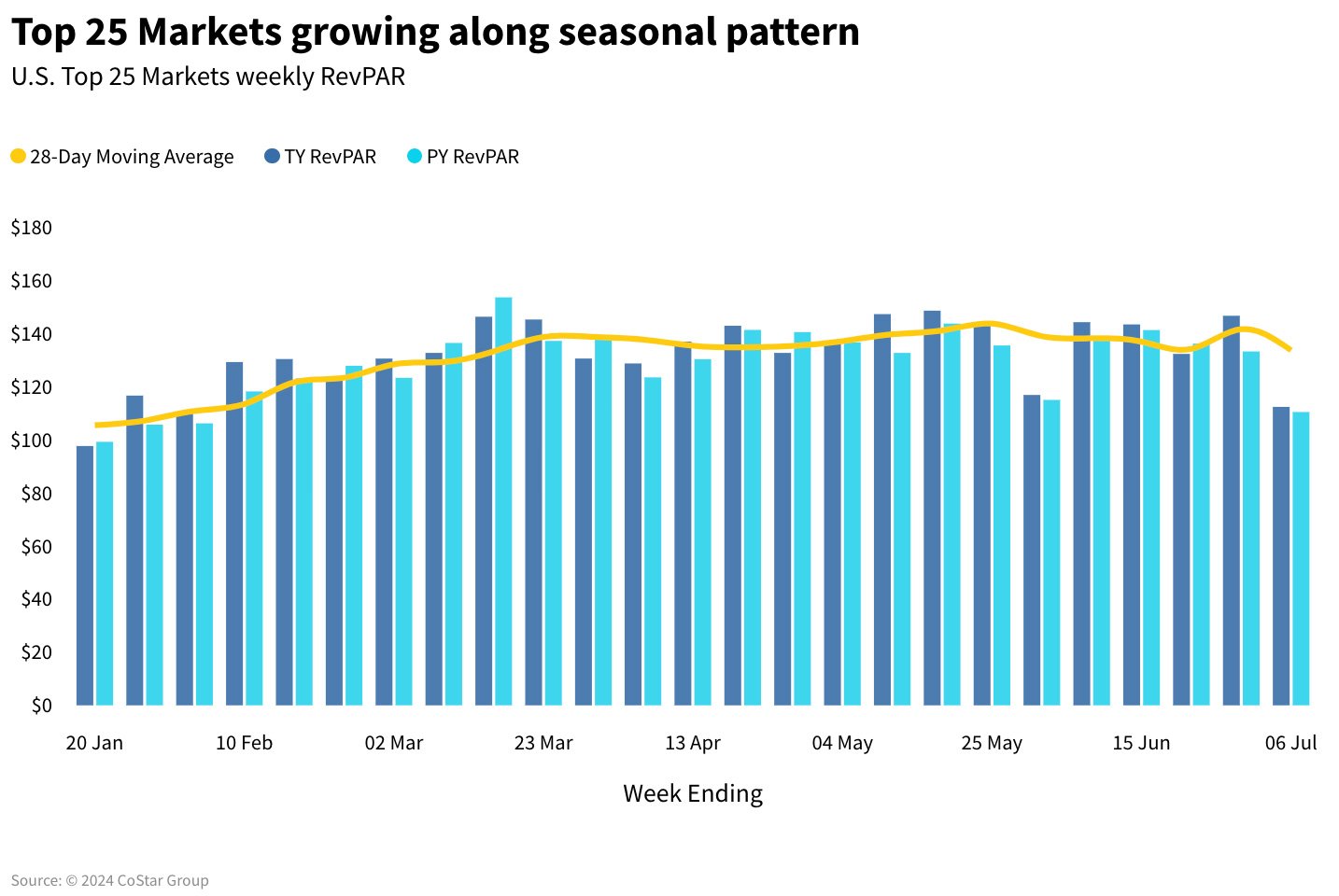

Top 25 Markets still driving industry RevPAR growth

In the Top 25 Markets, RevPAR increased 1.8% YoY led by ADR (+1.0%) and occupancy rising by half a point. In the remaining markets, RevPAR decreased (-1.8%), entirely due to falling occupancy (-1.1ppts) as ADR was flat.

Eleven of the Top 25 Markets saw weekly RevPAR increase by more than 4% YoY with six seeing double-digit growth. New Orleans saw the largest increase (+56.1%) followed by Seattle, Houston, Philadelphia, Denver, and Oahu. Four of these markets, New Orleans, Seattle, Philadelphia, and Oahu, benefitted from strong group performance during a traditionally slow week for groups.

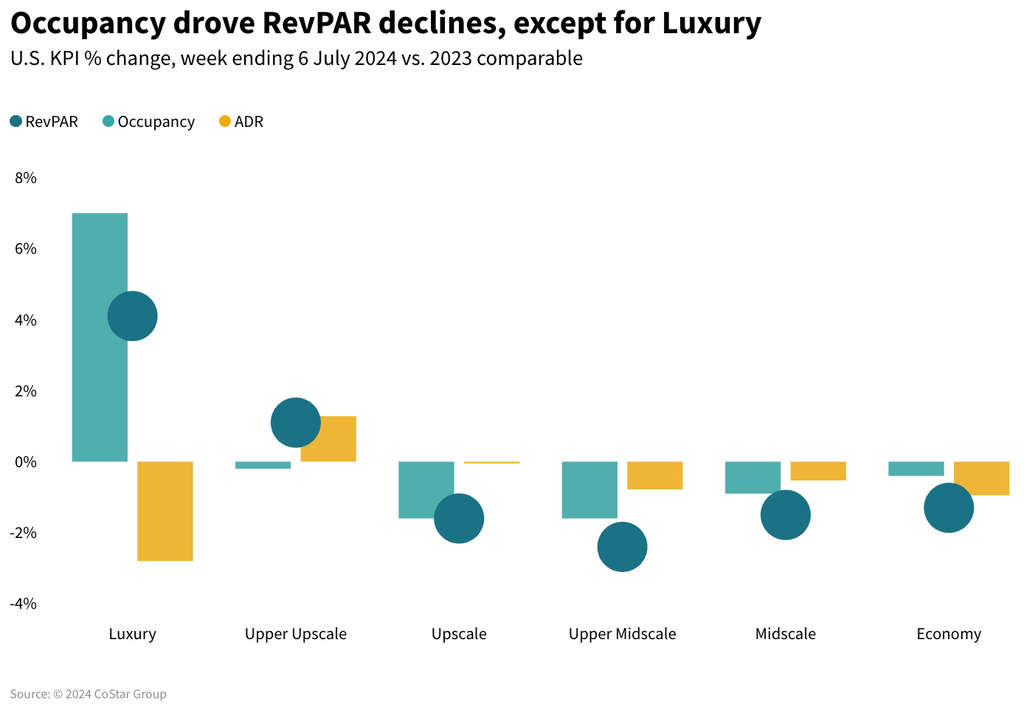

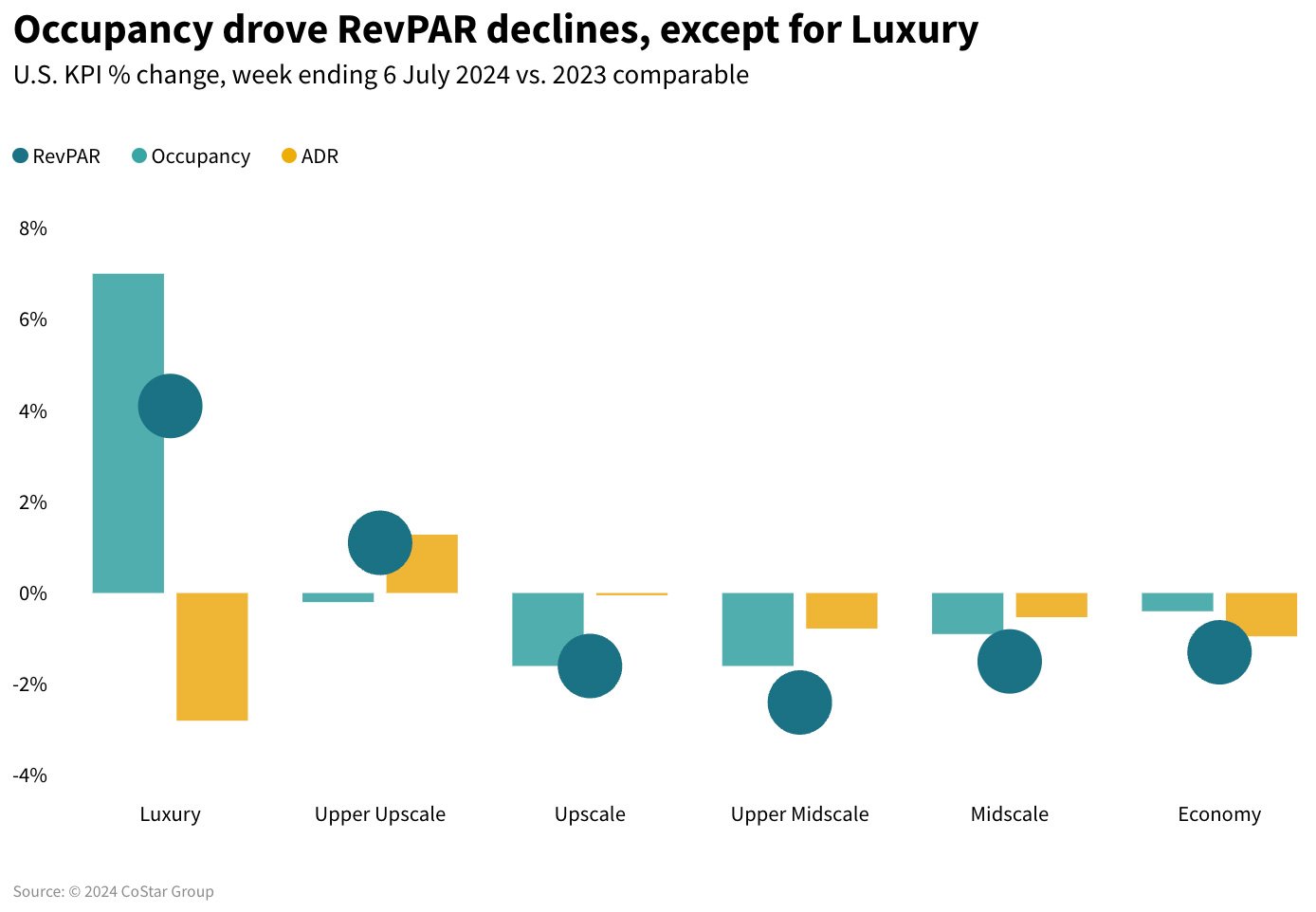

All but the top chain scales posted declines during the holiday week

Room demand by chain scale remained bifurcated. Luxury saw its highest room demand of any previous July 4th week while Economy posted its lowest. Even though Luxury demand was at a record high for the holiday week, Luxury occupancy was still only the 16th best of the past 25 years behind the record set in 2015 (60.2% vs 69.5%). Room demand for Upscale and Upper Midscale was the fourth highest for the holiday week behind the level seen in 2021. For Upper Upscale, demand was the third highest behind 2019.

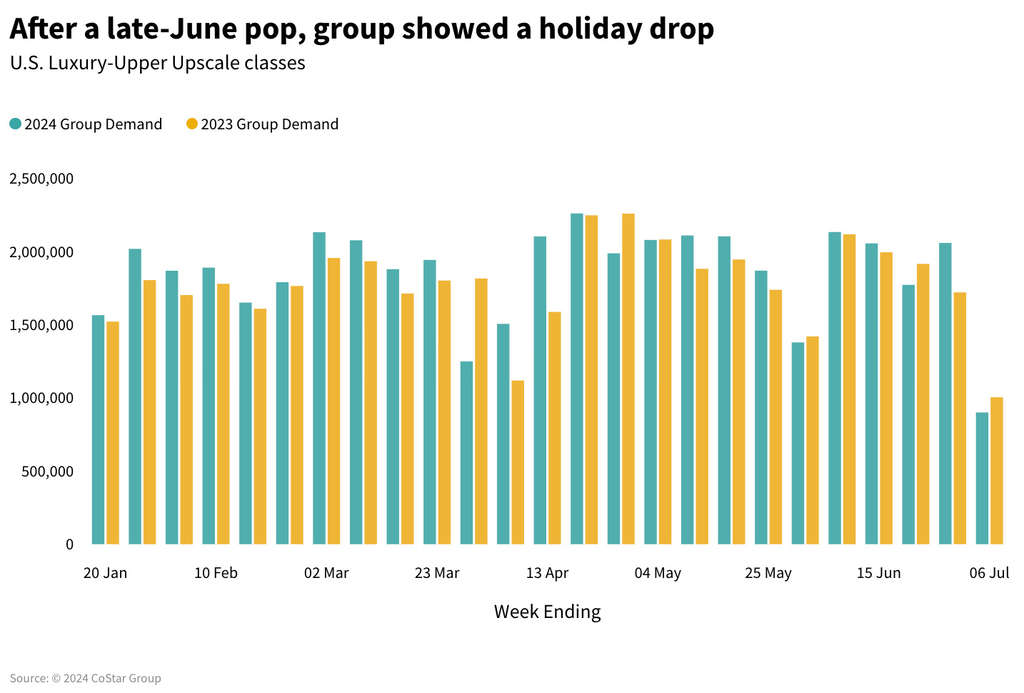

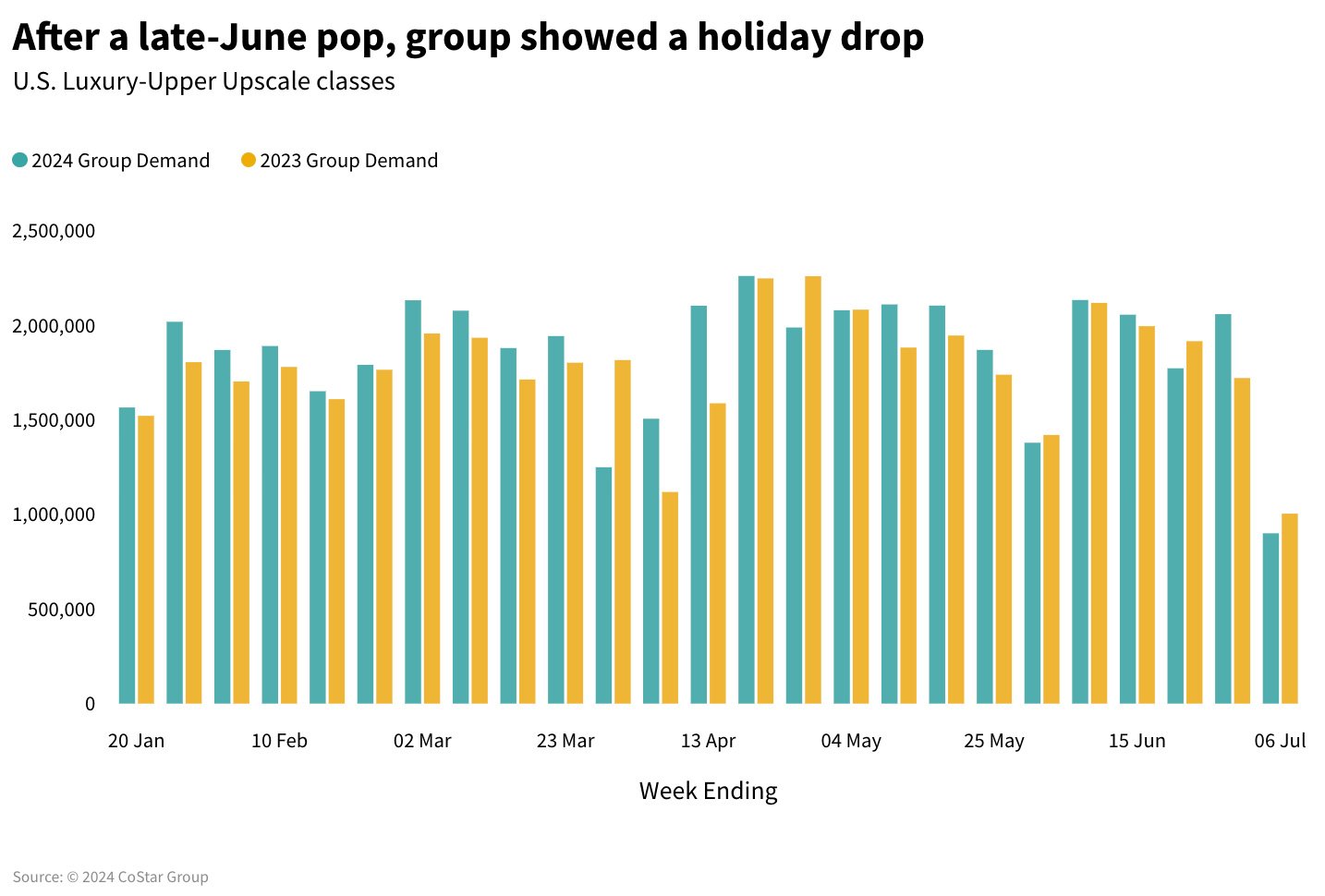

Group demand impacted by the holiday shifts

Luxury and Upscale hotel group demand decreased 10.3% compared to the same week last year following an exceptional increase the previous week of 19.6% YoY. The strong group seen in the previous week was the result of being bookended by the Juneteenth and July 4th holidays. Group demand is expected to ramp back up in the next two weeks before the August slow-down followed by a strong fall, which is the most popular time of year for conferences and events. Group ADR continued to strengthen, up 3.2% during the holiday week and 7% in the previous one.

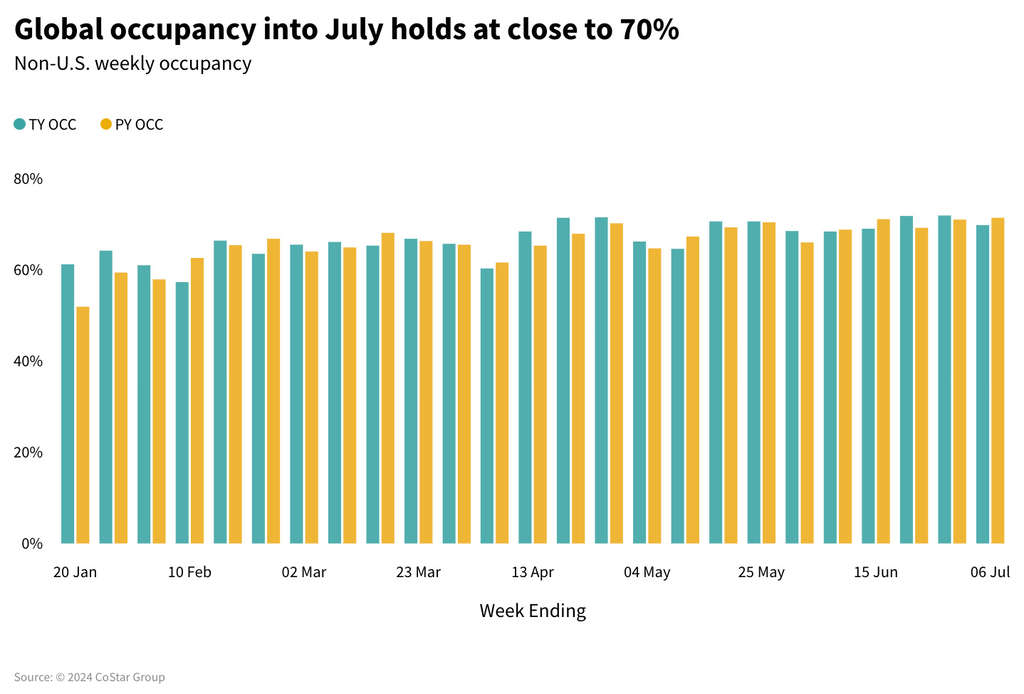

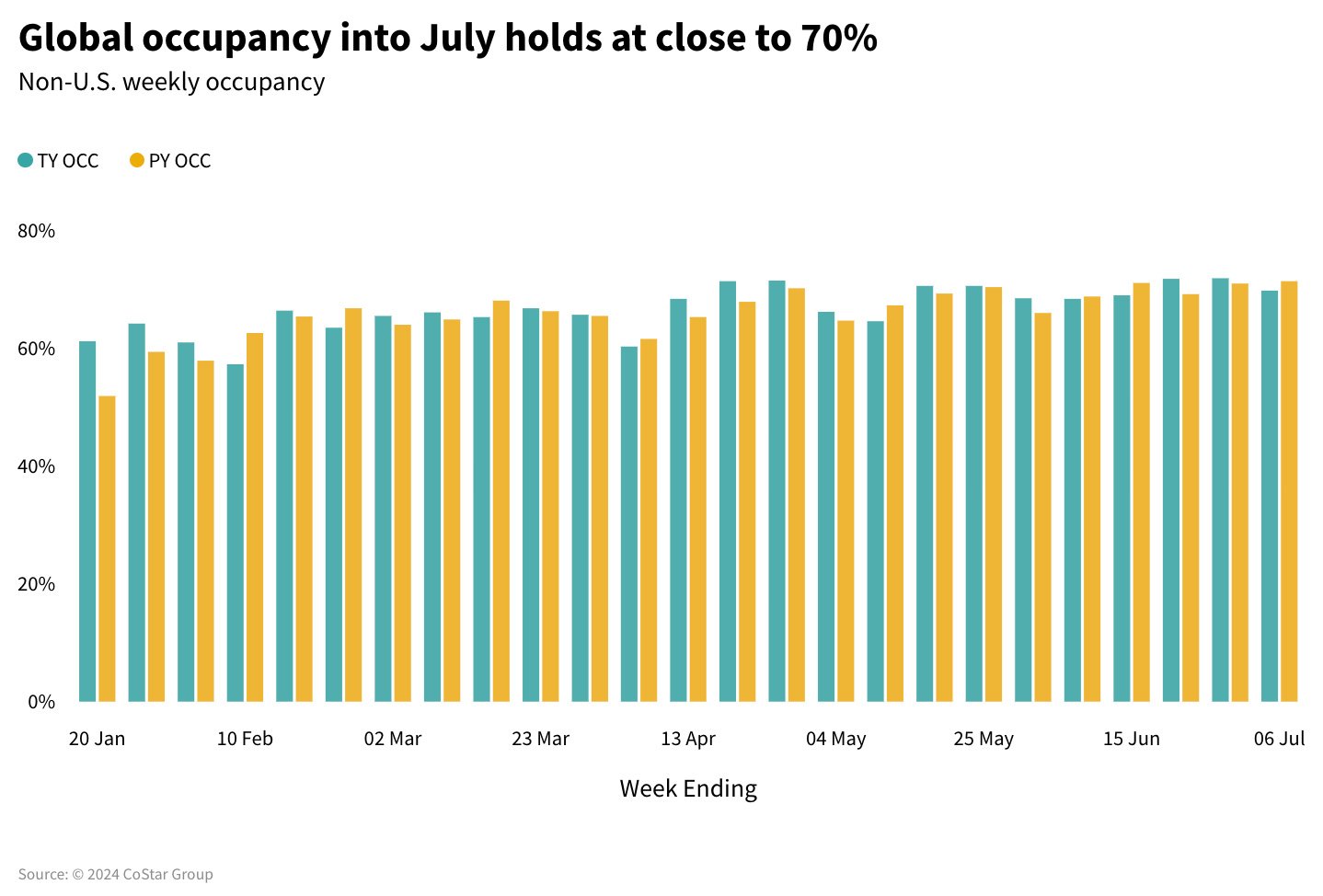

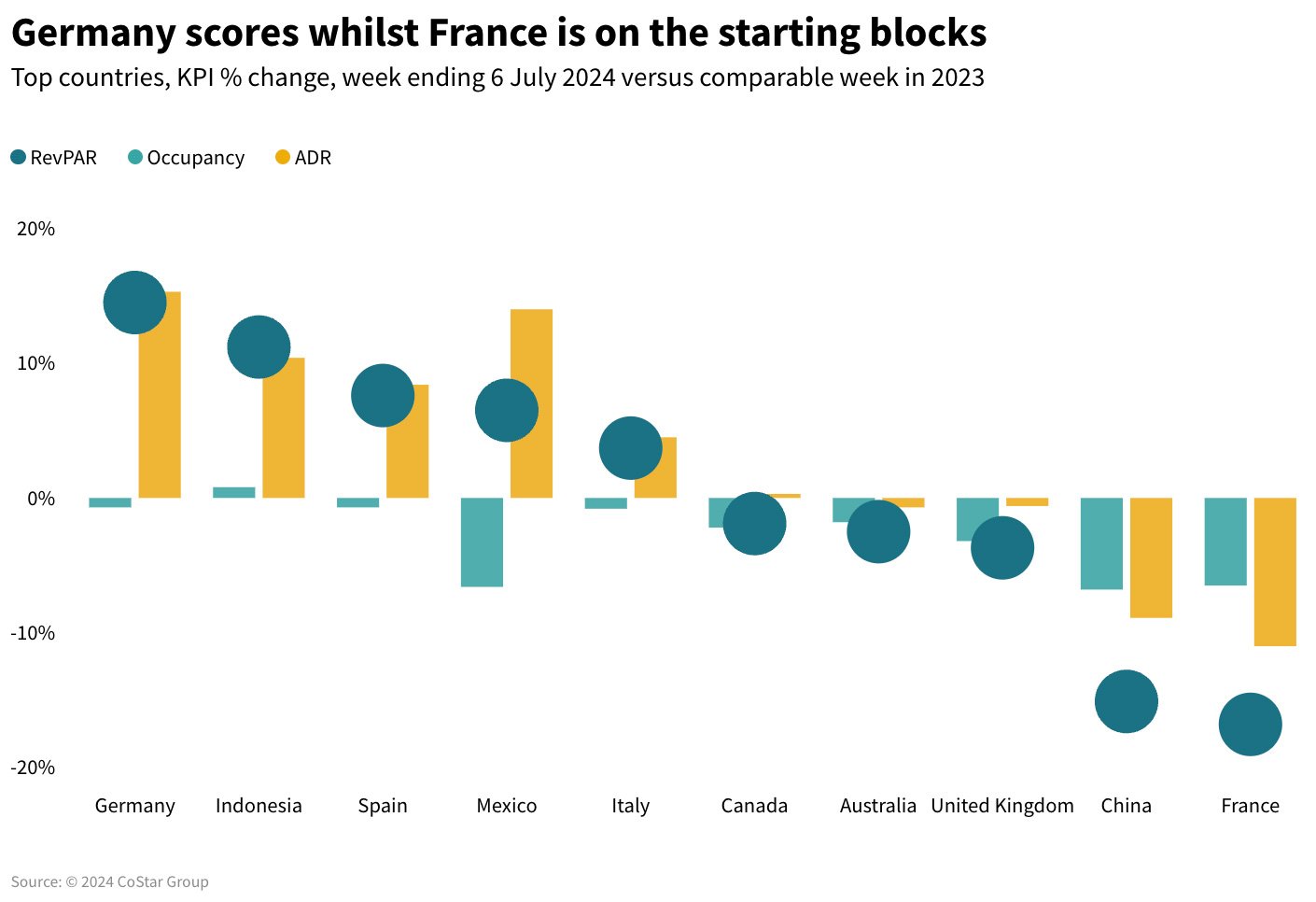

Global ADR grew YoY for the 23rd week

Global occupancy (69.8%) fell 1.6ppts with many of the largest countries, based on supply, recording declines. ADR, however, continued to advance, up 2%, which was insufficient to offset the occupancy decrease resulting in a 0.4% RevPAR decline.

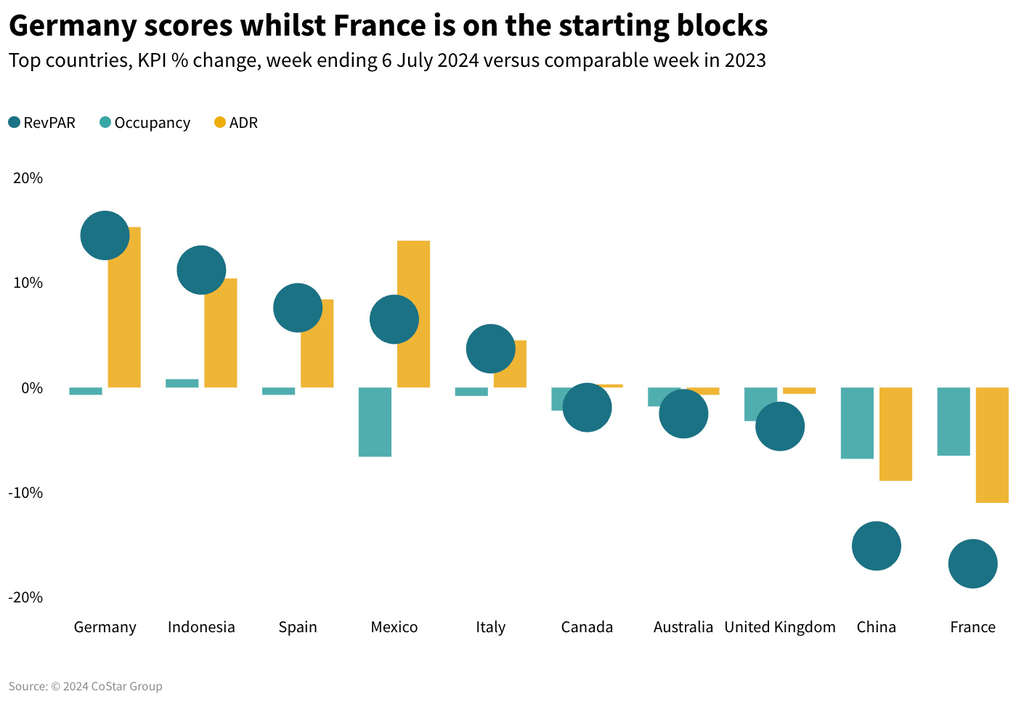

As host to the Euros, Germany led in results among the largest hotel markets with a 14.5% RevPAR gain. The gain was all ADR (+15.3%) while occupancy was down slightly (-0.5ppts). Düsseldorf, which hosted two knockout stage matches, saw the largest gains with RevPAR up 90.5% via ADR (+58.4%) and occupancy growth.

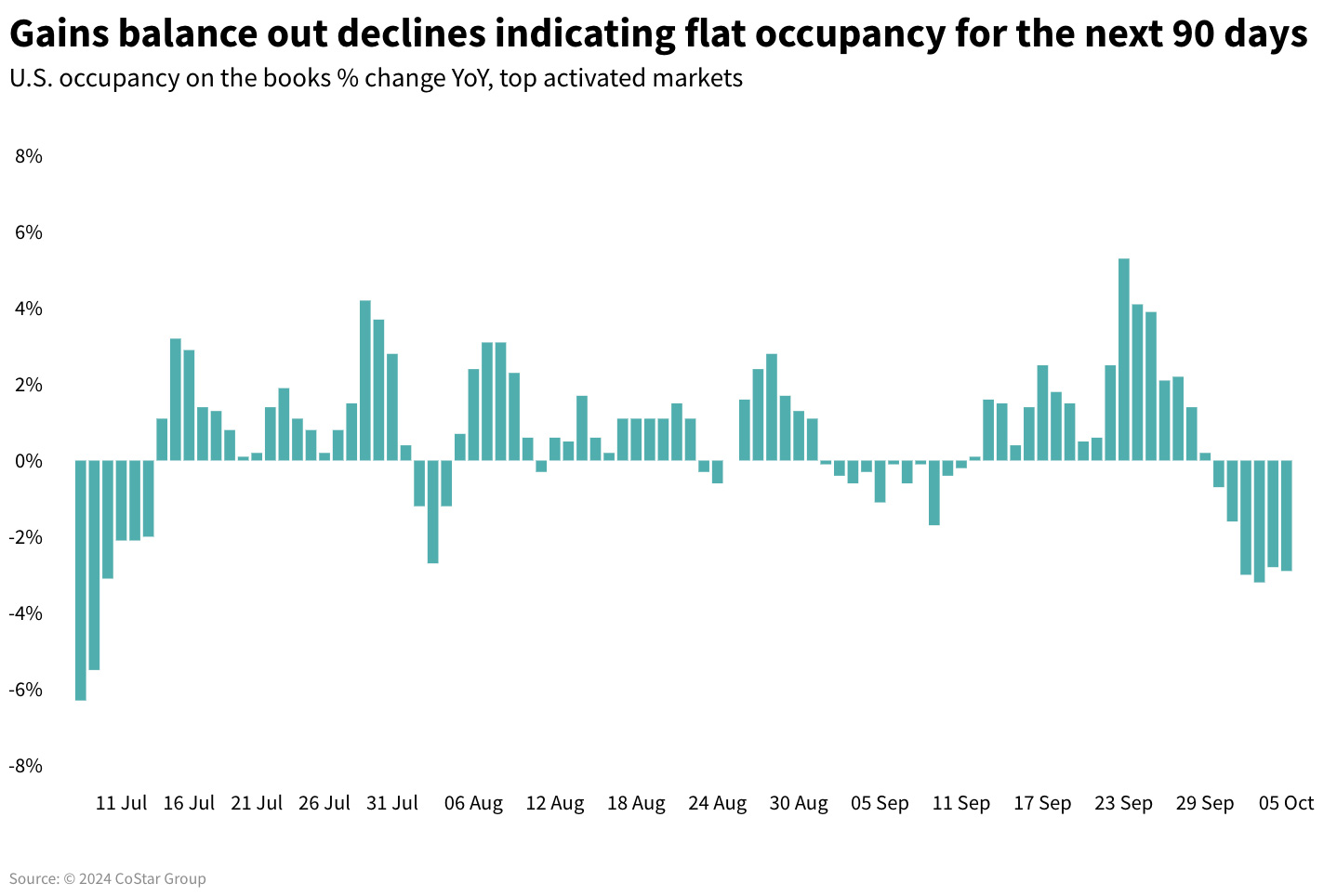

At the other end of the performance spectrum, France continued to see demand displacement with just under three weeks until the Olympics, experiencing a RevPAR decline of 16.8%, driven by decreases in both ADR (-11%) and occupancy (-5.0 ppts). This is particularly evident in Paris, where the most recent week's occupancy fell 10.5ppts to 72.0%, ADR dropped 25%, and RevPAR decreased by 34.5%. Looking ahead, significant performance gains are expected during the Olympics with occupancy on the books as of 8 July at 81%, which was 28% higher than at the same time last year.

Looking ahead

The next week of data should show post-July 4th recovery of business and group demand along with continued strength from leisure. TSA airport screenings continued to break records with Sunday, 7 July showing the highest number of daily airport screenings. Numerous research companies are reporting strong summer travel. According to Future Partners, 73.5% of American travelers said they were likely to take at least one trip between June and August. Longwoods International reported that of American travelers, 94% plan to travel in the next six months, the highest percentage in 2024. Of concern with all this optimism is that the hotel industry hasn’t seen the same level of growth as the air travel and surveys suggest. The industry is facing headwinds created by the continued growth of short-term rentals along with the travel outbound/inbound travel imbalance. We expect occupancy to reach its yearly peak over the next two weeks followed by seasonal slowing as the school year begins, starting in the southern U.S.

September and October, the most popular months for conventions and conferences, will see strength from group demand followed by November and then December, the slowest month of the year. A similar pattern is expected for the remainder of the world.

About STR

STR provides premium data benchmarking, analytics and marketplace insights for the global hospitality industry. Founded in 1985, STR maintains a presence in 15 countries with a North American headquarters in Hendersonville, Tennessee, an international headquarters in London, and an Asia Pacific headquarters in Singapore. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), the leading provider of commercial real estate information, analytics and online marketplaces. For more information, please visit str.com and costargroup.com.