STR Weekly Insights: 4-10 August 2024

Countries/markets mentioned:

- United States: Atlanta, Boston, Chicago, Denver, Houston, Las Vegas, New Orleans, New York City, Oahu, Anaheim (Orange County)

- Global: China (Shenzhen), France (Île-de-France, Paris)

Highlights

- End-of-summer lift for the U.S., but not enough to keep up with inflation

- Economy chain scale RevPAR positive for first time in months

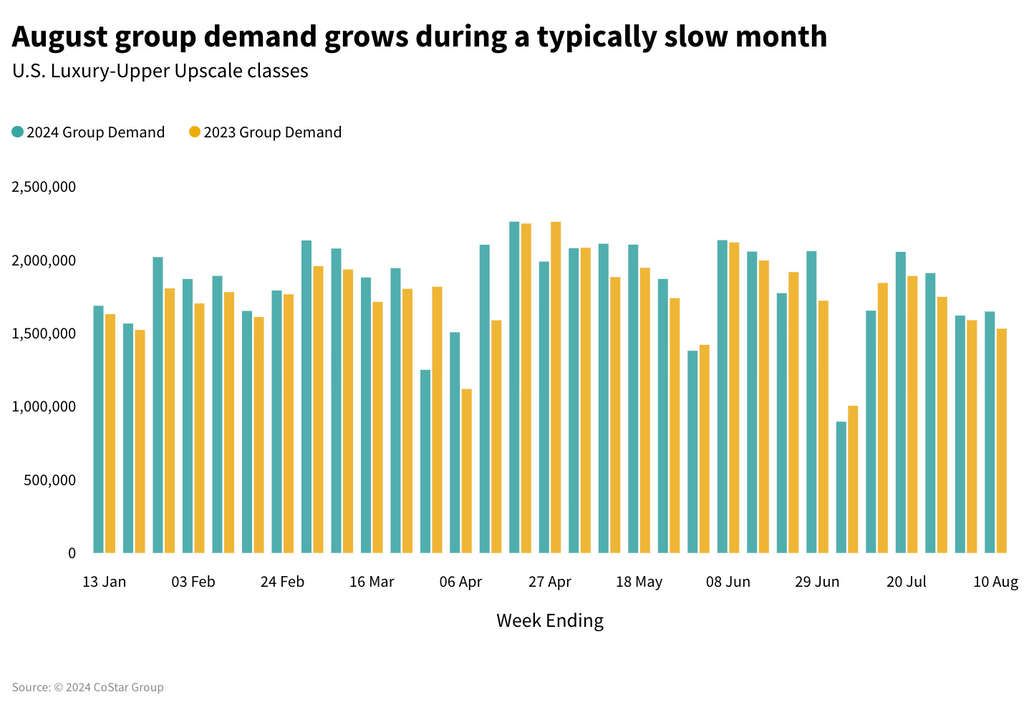

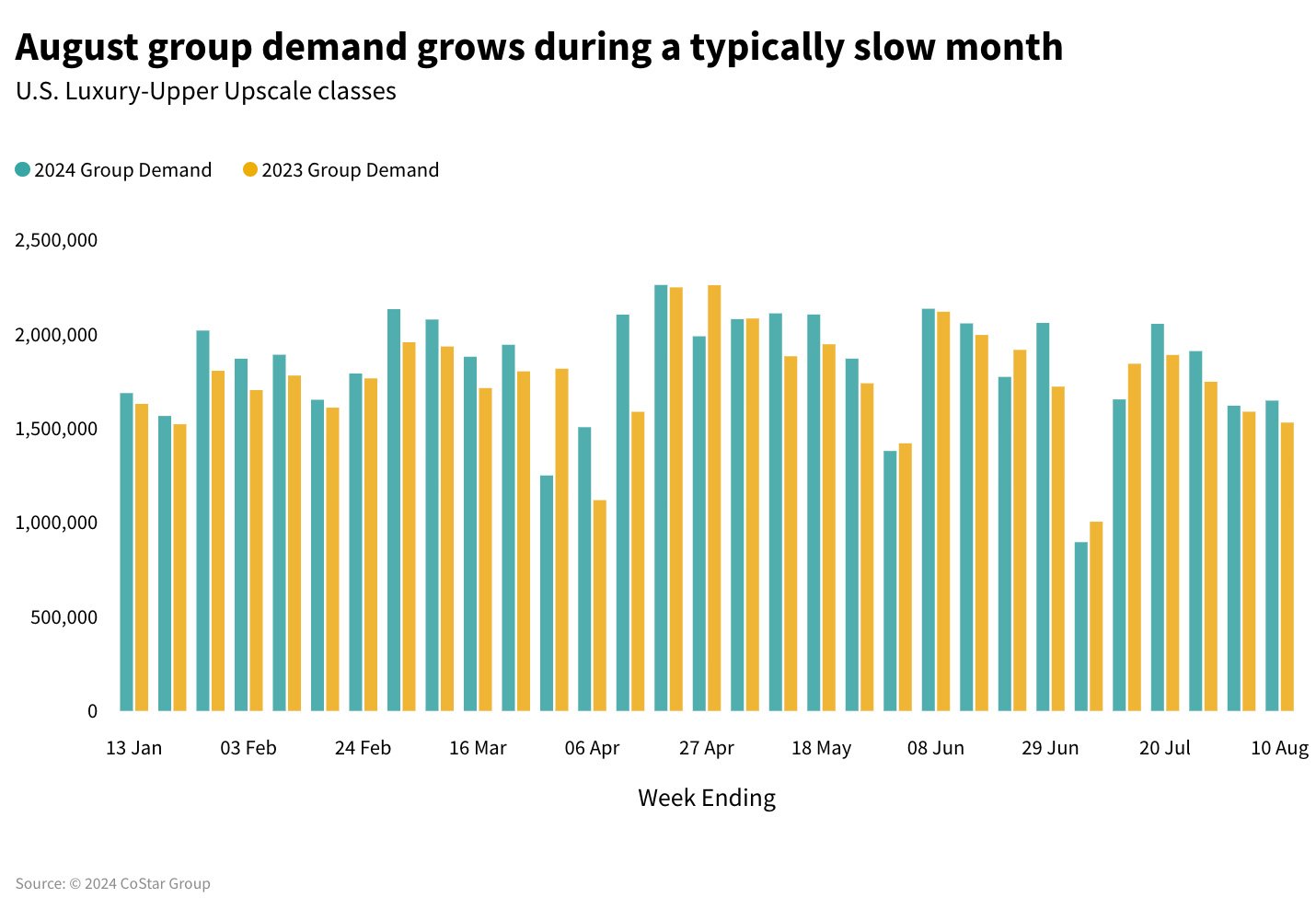

- Healthy group demand and ADR continues

- Gold medal performance for Paris hotels

- China hotel performance slows in markets across the country

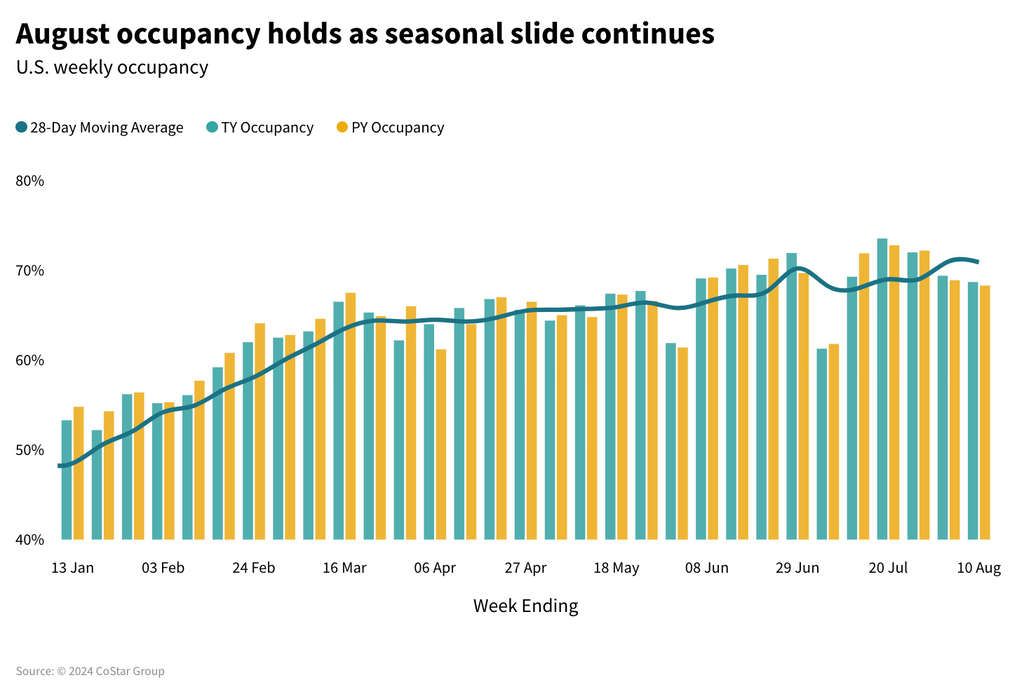

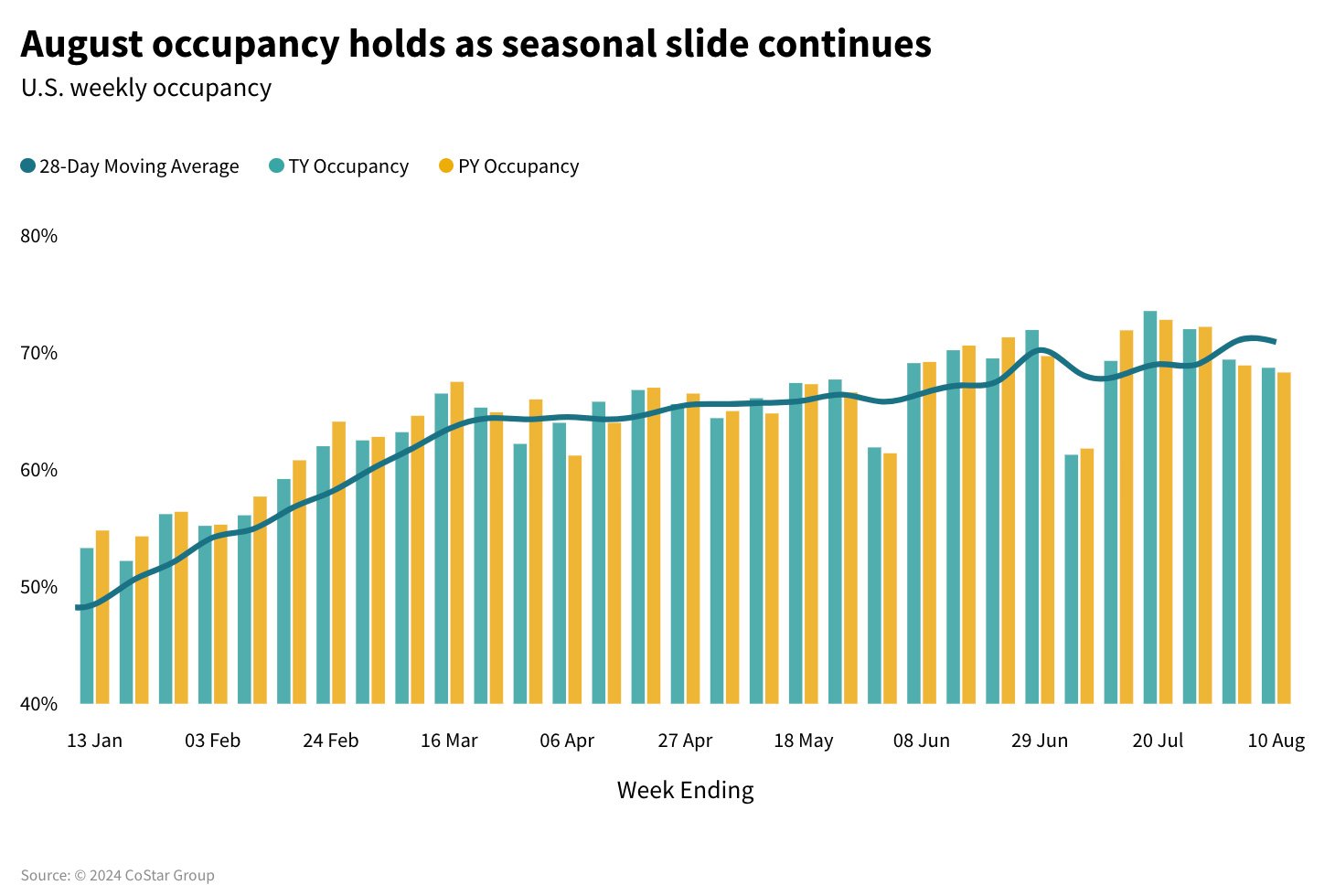

Travelers are squeezing the last drops out of summer as U.S. hotel room demand strengthened year over year (YoY) for the fourth straight week. Occupancy has increased in three of those weeks with growth softened by a small supply increase. Average daily rate (ADR) has continued to rise, pushing RevPAR gains for the past four weeks, but at a rate below the level of inflation.

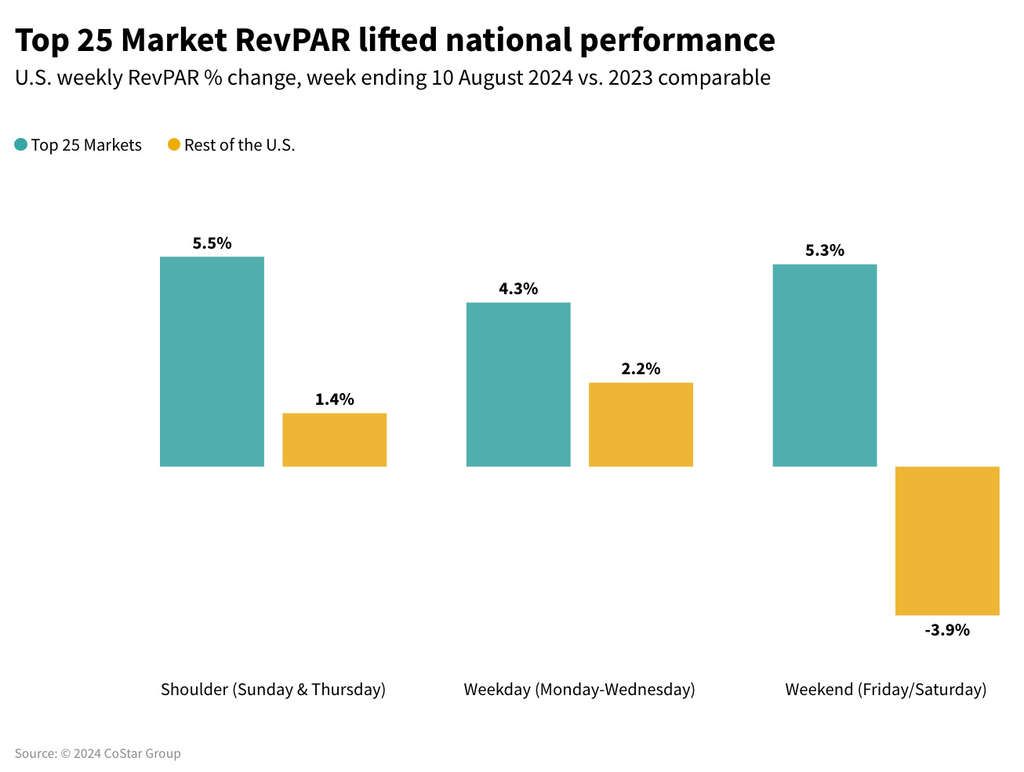

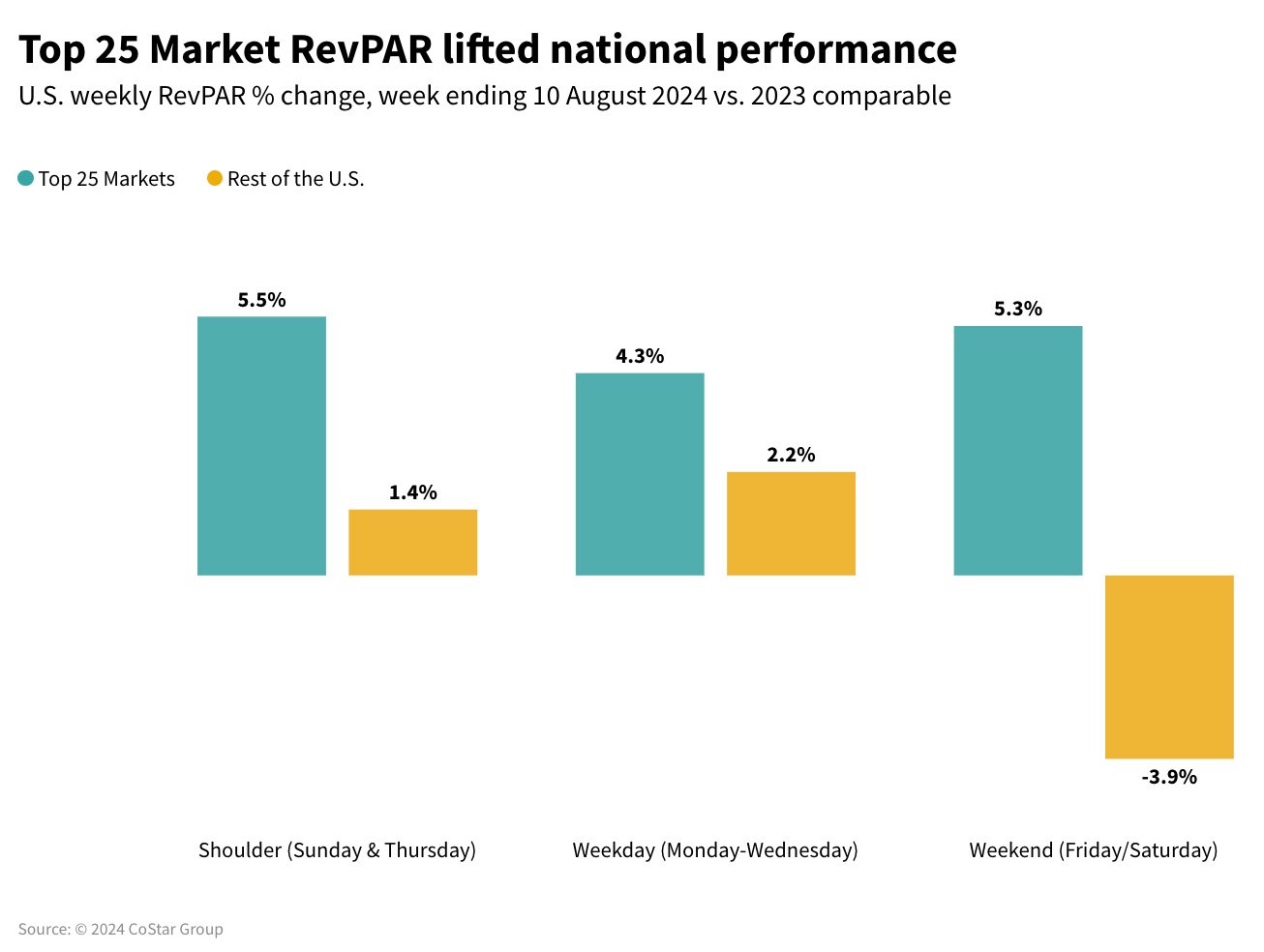

The Top 25 Markets are primarily responsible for the RevPAR lift, which is a pattern seen for most of the year while the remaining markets have been flat to down. Also driving performance this week was strong summer group demand, which is typically slow during the summer season.

Improving performance continues following summer’s peak

U.S. RevPAR increased for the fourth week in a row, up 1.9% YoY due to increasing ADR (+1.4%) and occupancy (+0.4 percentage points). While increasing, RevPAR remained below the rate of inflation. The Top 25 Markets (+4.9%) drove RevPAR, as occupancy rose 2.0% and ADR increased 2.1%. That gain in the major metros was offset by flat RevPAR (-0.1%) across the rest of the country. The Top 25 Markets saw strong performance Tuesday through Saturday with the largest YoY increases on Wednesday (+8.0%), Thursday (+11.3%), and Friday (+7.8%).

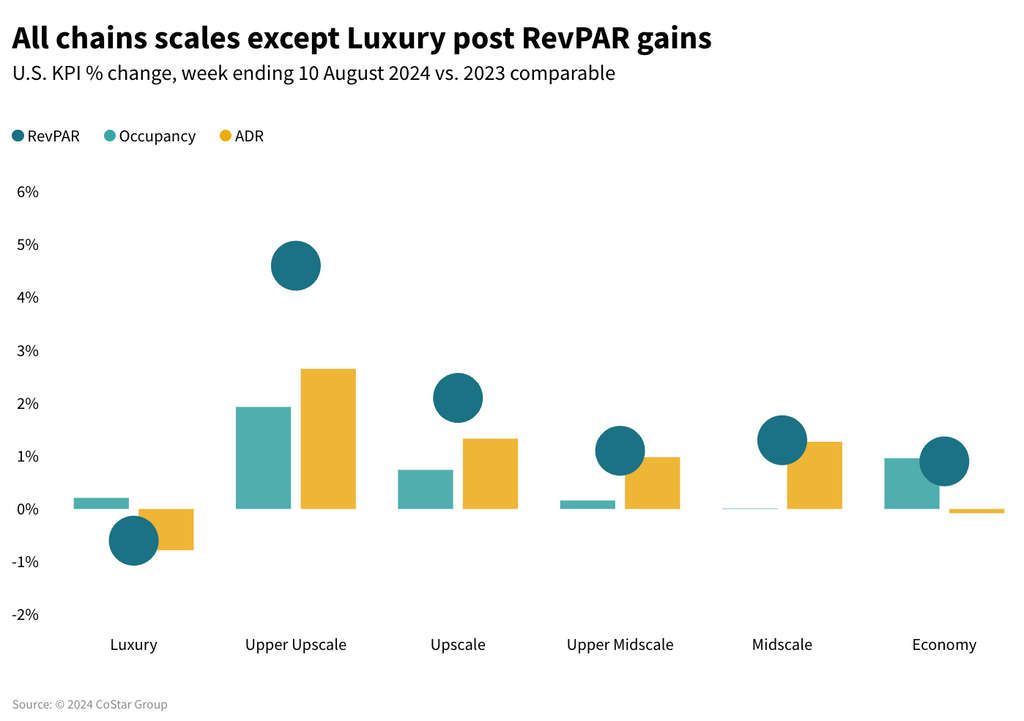

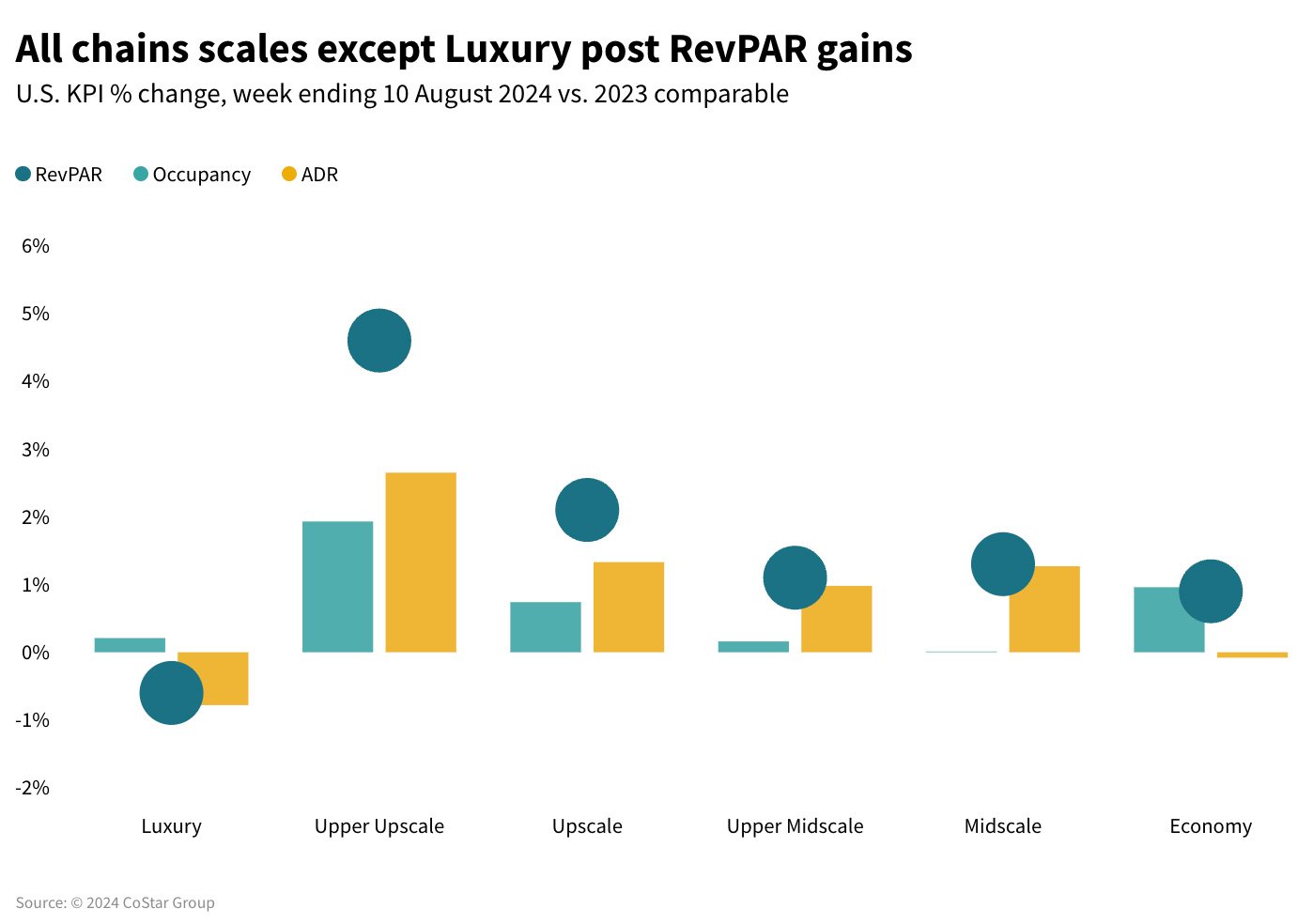

Most chains scale posted RevPAR gains

All chain scales, except Luxury, posted RevPAR growth for the week, including Economy (+0.9%). This was Economy’s first weekly increase since April and only the third gain since May 2023. All branded chain scales recorded occupancy increases, while ADR growth was the primary driver of RevPAR for Midscale through Upper Upscale. Upper Upscale saw the largest RevPAR gain (+4.6%), a result of rising occupancy and ADR. Upscale through Midscale followed with RevPAR gains between +1.3% and +2.1%. Luxury’s slight RevPAR decline (-0.6%) was entirely due to ADR.

A summer of growth for Houston

Double-digit RevPAR growth was seen in eight of the Top 25 Markets with Houston (+47.2%) earning top honors. Markets seeing 20%+ RevPAR growth were Chicago, St. Louis, Denver, and New Orleans. Rounding out the double-digit list were Seattle, Boston and New York City. The Houston market has posted double-digit RevPAR gains in 13 of the past 14 weeks with the most recent week’s results the highest yet. Strong group demand from conferences and sporting events, along with earlier impacts from Hurricane Beryl, has lifted performance in the market. This growth was seen across almost all of Houston’s submarkets (9 out of 11).

Healthy group demand and ADR continues

Group demand in Luxury and Upscale hotels has increased for the past four weeks producing an average increase of 6.9% YoY. In the most recent week, group demand was up 7.6%, and ADR advanced 3.4%. As with the industry overall, the Top 25 Markets were responsible as group demand was up 14.4% while ADR increased a modest 1.6%. Across the other markets, demand was more moderate, but ADR grew a robust 5.8%.

Ten of the Top 25 Markets experienced group demand gains of more than 20%, including Atlanta, Chicago, Denver, Las Vegas, New Orleans, New York, Oahu, Anaheim (Orange County), St. Louis, and Seattle.

Transient performance across Luxury and Upper Upscale hotels softened with demand down 0.4% and ADR up 1.4% YoY. Across the Top 25 Markets, ADR was stronger, up 2.6%, while demand was weaker, down 1.2%.

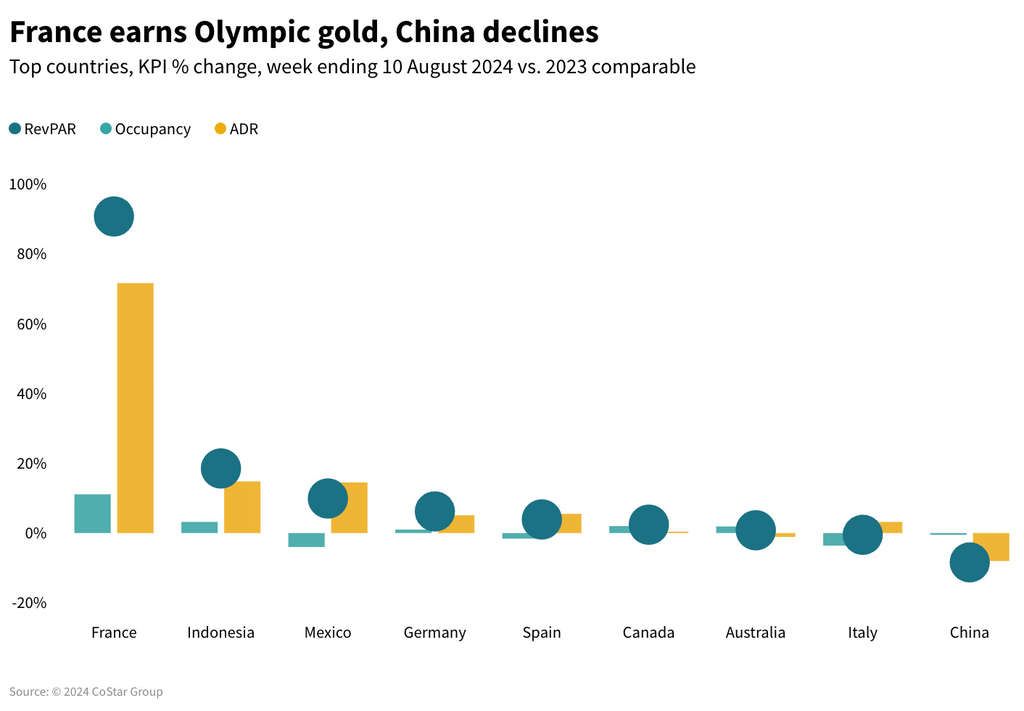

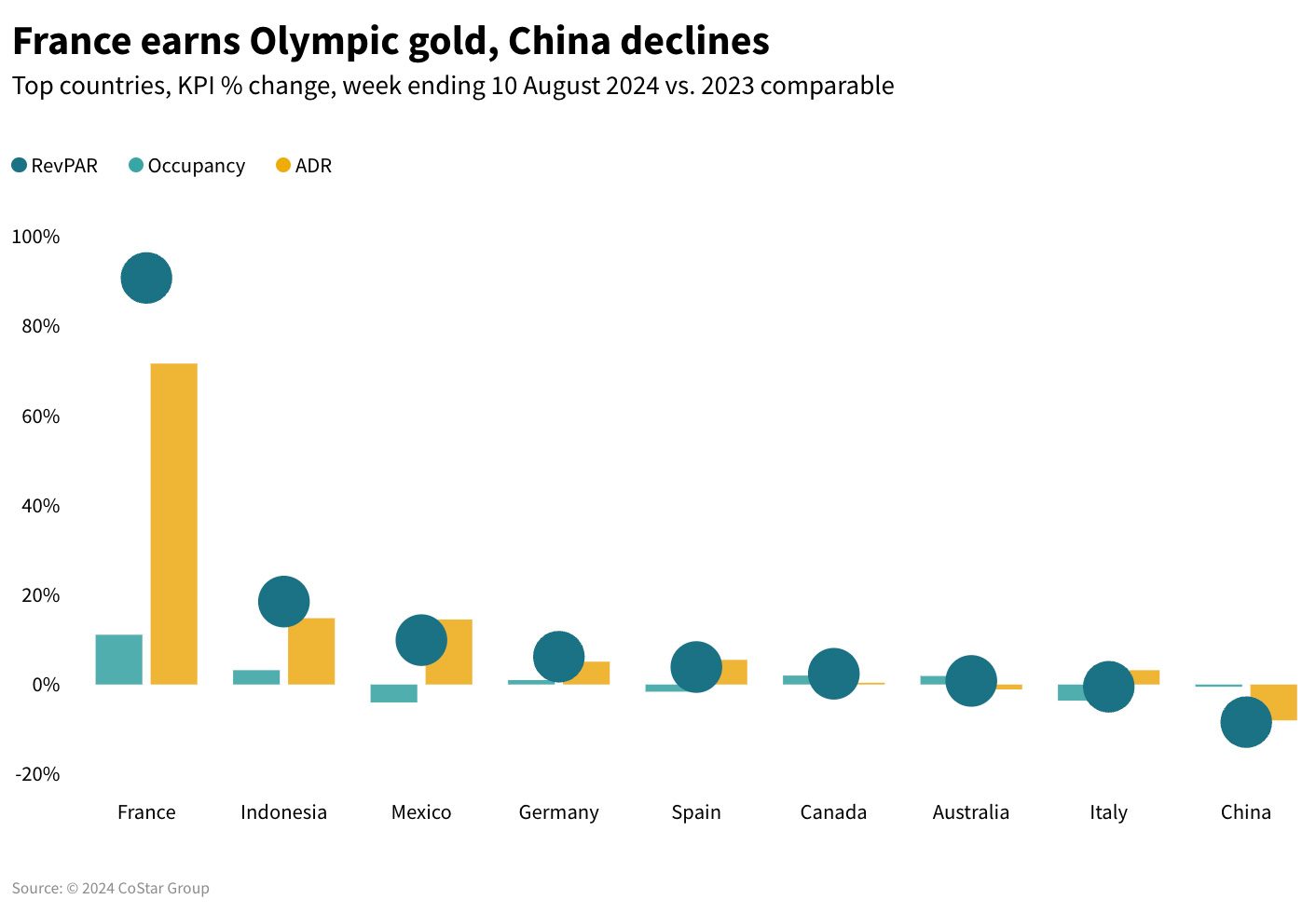

A tale of two countries with a gold medal performance in France and a slowdown in China

Week two of the Olympics provided France with more hotel performance gold. Paris RevPAR increased 195.9% following the previous week’s record-breaking gain of 207.2% growth. Occupancy increased 16.9 ppts with ADR up 137.8%. Friday night produced the highest RevPAR of the week (US$735), while Sunday showed the largest RevPAR increase (+224.7%). Th Olympic impact extended to the surrounding Île-de-France region, which saw RevPAR grow 169.1% YoY, lifted primarily by ADR, although occupancy also increased.

Performance in China has been slowing over the past year with the last four weeks showing YoY decreases in both occupancy and ADR, with the latter was mostly responsible for the continuing RevPAR fall. This decline has been seen across most of China’s submarkets. Of the top 10 largest submarkets, all but Shenzhen posted negative performance comparisons over the past four weeks. Economic challenges across the country as well as potential “revenge travel” fatigue are probable contributors to this weak performance. At -8.4%, the most recent RevPAR decline was better than the -11%+ seen in the prior two weeks.

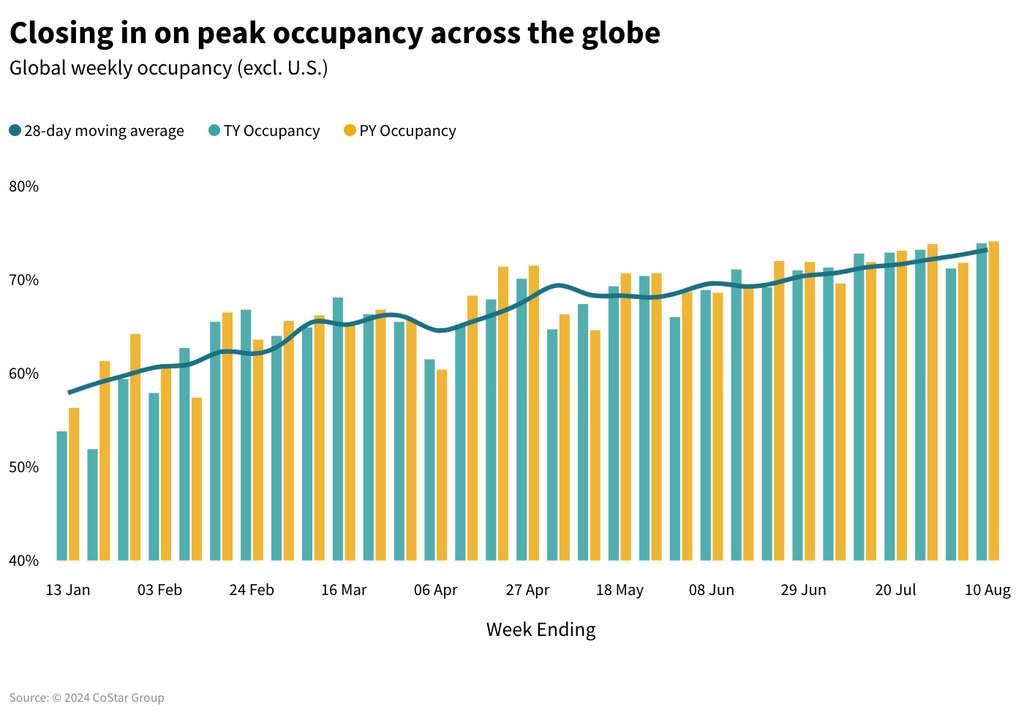

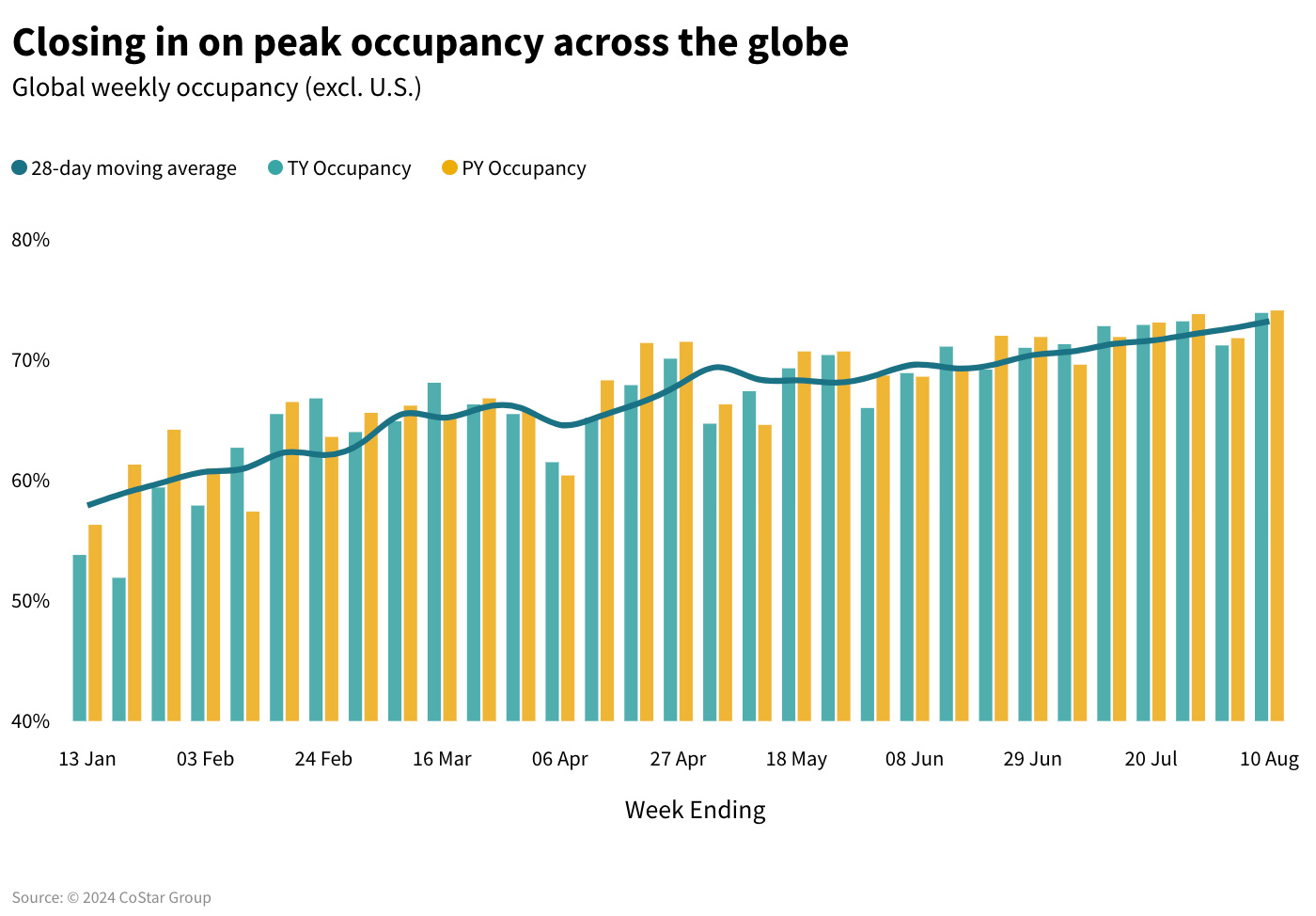

Occupancy across the globe is slowing year over year and may have hit its yearly peak, which tends to occur a couple weeks after the U.S. due to later school start dates.

Looking ahead

August is off to a strong start after a lackluster July. This summer’s solid group performance will continue to wane as is typical this time of year before ramping up in September when it will be clear whether the seemingly unending strength of group demand will continue. Group ADR is softening, which is encouraging for event planners but not for hoteliers. Business transient will also increase in September and the strong weekday performance seen all summer serves as a good indication that business travel will continue.

Global performance will start to show a seasonal slowing as summer comes to an end. France, and Paris in particular, may see an uptick in travel with tourists and business travelers, who avoided the area during the Olympics, returning.

All indications are that China will continue to see soft performance. For the rest of the world, performance is expected to slow.

July 2024 international travel statistics continue to show a lopsided balance with more Americans traveling internationally than their international counterparts visiting the U.S., and we expect this trend will continue into the fall in the northern hemisphere.

*Analysis by Isaac Collazo, Chris Klauda.

About STR

About STR

STR is the global leader in hospitality data benchmarking, analytics and marketplace insights. Founded in 1985, STR maintains a robust global presence with regional offices strategically located in Nashville, London, and Singapore. In October 2019, STR was acquired by CoStar Group, Inc. (NASDAQ: CSGP), a leading provider of online real estate marketplaces, information and analytics in the commercial and residential property markets. For more information, please visit str.com and costargroup.com.