STR Weekly Insights: 15-21 October 2023

Countries included: Chile, Ireland, South Korea, United Arab Emirates, United Kingdom, and the United States.

U.S. Performance

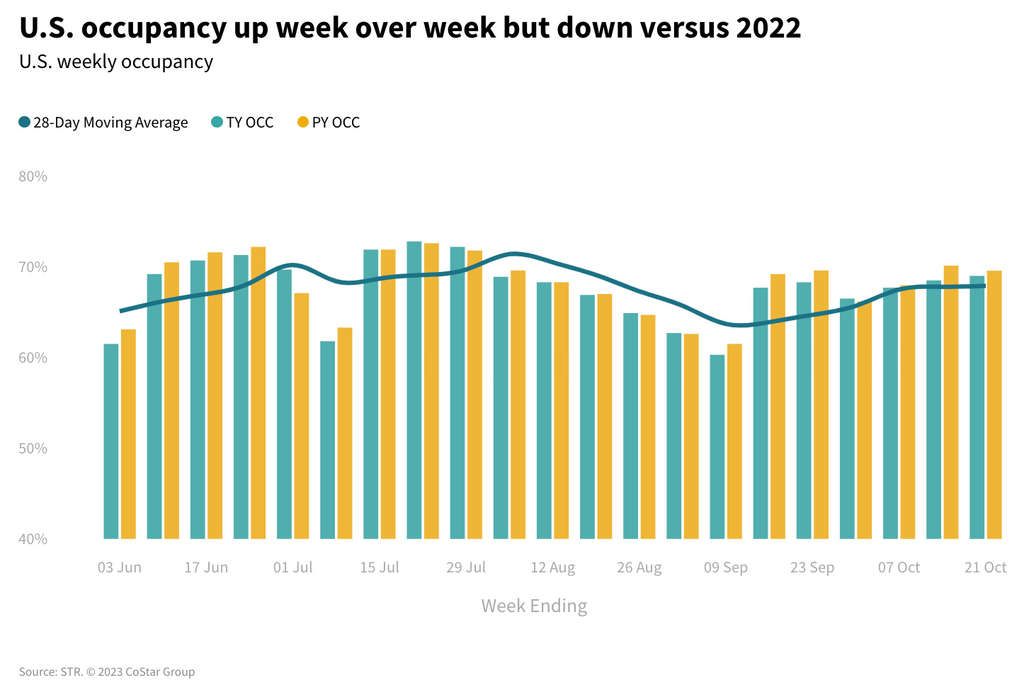

U.S. hotel industry occupancy increased 0.5 percentage points (ppts) from the previous week to 69.0%, which was expected because this week was free of holiday and religious observance impacts, however, compared to last year it was down 0.6ppts. This is the third week in a row occupancy has declined year over year (YoY). On the upside, ADR increased 3.8%, its fifth consecutive week above 3%, resulting in a 2.9% RevPAR gain.

The occupancy decline continued to be led by economy class hotels, which accounted for 77% of the demand decrease among the three classes (Upper Midscale, Midscale and Economy). Luxury, Upper Upscale and Upscale classes all saw weekly demand growth with occupancy increasing in the latter two.

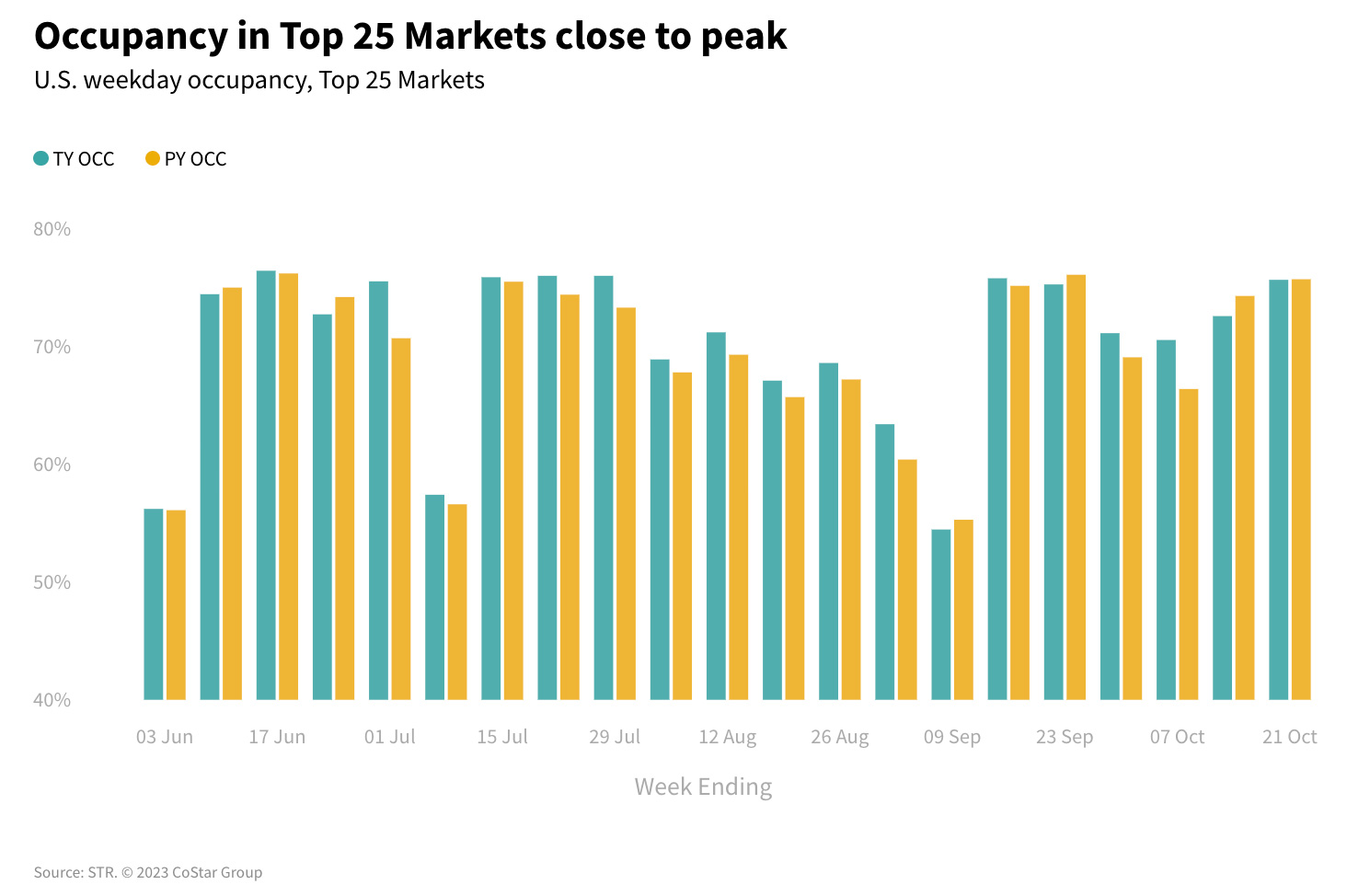

Among the Top 25 Markets, which have had stronger performance this year, occupancy was flat

(-0.1ppts YoY) this week following last week’s decline of 1.9ppts. ADR increased a healthy 4.7%, netting a RevPAR gain of 4.5%. In the remaining markets, occupancy continued to decrease as it has for the past 16 weeks. As stated previously, we believe this year’s performance among non-Top 25 Markets represents a return to normal.

The interplay of strengthening weekdays (business) and softening weekends (leisure) has been observed all year and this week was no exception. Weekend occupancy was down the most (-1.0ppts) followed by the shoulder period (-0.8ppts). Weekdays were only slightly down in occupancy (-0.2ppts). Among the Top 25 Markets, all three dayparts were less impacted but mimicked the national pattern with weekend occupancy down the most (-0.4ppts), followed equally by shoulder and weekday periods (-0.1ppts). The rest of the U.S. saw weekend and shoulder periods down 1.3ppts and 1.2ppts, respectively, as weekday occupancy stayed nearly flat (-0.2ppts YoY).

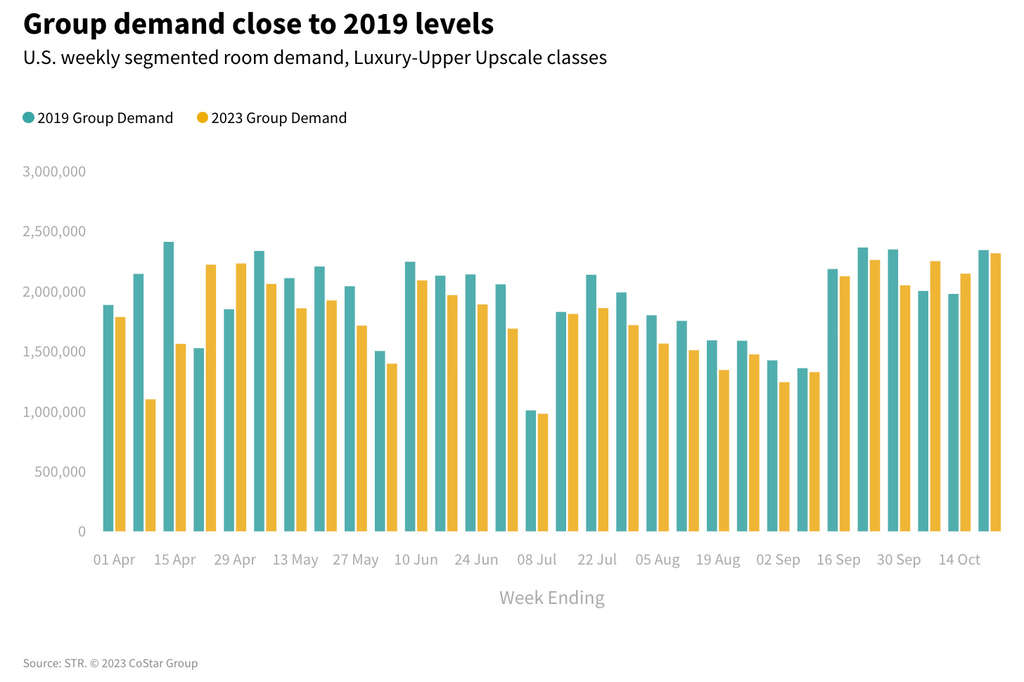

The increase in group meetings and events is another trend reflecting the normalization of travel. Group demand among Luxury and Upper Upscale hotels reached their highest level since the pandemic, at 2.3 million rooms, which is just 1% (27,000 rooms) shy of the same week in 2019. Factoring in supply, this week’s group occupancy, at 27.2%, is 2.4ppts below 2019. Year over year, group demand grew 1%, while week over week it grew 7.9%. Group ADR, at US$266, increased 5.9ppts WoW and 1.9ppts YoY. The Top 25 Markets posted the largest group occupancy increase YoY, with Seattle (+12.2ppts), Atlanta (+8.3ppts), Philadelphia (+5.5ppts) and Oahu (+5.3ppts) showing the highest lifts in the metric. Upper Upscale class hotels, those most likely to host group events, posted their third highest room demand since early March 2020.

This week’s occupancy was highest in Las Vegas (89.2%) followed by New York City (89.1%), Boston (87.7%), Gatlinburg/Pigeon Forge (82.9%), and Austin (82.8%). Events, such as Austin’s Formula One Grand Prix; conventions, and seasonal trips were responsible for the high occupancy in those markets.

Global Performance

Global occupancy, excluding the U.S, grew to 71.3%, increasing 2.3ppts WoW and up 7.6ppts from a year ago. ADR was also up year over year (9.4%) but down 2% over the previous week. RevPAR grew 22.5% YoY to US$102, continuing the streak of 20%+ growth seen nearly all year. The top 10 countries, based on supply, continued to see strong performance, with this week’s occupancy reaching 73.8%, up 10.8ppts from a year ago, with ADR and RevPAR growing 7.9% and 26.3%, respectively.

The United Kingdom led the top 10 in occupancy (80.6%, -0.3ppts YoY). This is only the fifth time this year that the country has seen occupancy fall. Three of the declines can be attributed to the shift in holidays: school Easter break, the additional Bank holiday, and the Coronation period of King Charles. The other two (5 August & 21 October) were likely due to storms (Antoni and Babet) affecting parts of the country. Despite these slight decreases, ADR continued to grow leading to an average RevPAR growth of +11% over the past six months.

Outside of the top 10, the highest occupancies in each continent were:

- Chile (Americas), 73.1%, +11.1ppts YoY.

- South Korea (Asia Pacific), 83.1% +6.7ppts YoY.

- Ireland (Europe), 82.6%, +2.9ppts YoY.

- UAE (Middle East & Africa), 84.6%, +9.9ppts YoY. The country saw occupancy increase by 11.1ppts WoW, likely due to the UFC showdown week. UAE also had the world’s highest occupancy for the week.

Final thoughts

While strong global performance continues, the year-over-year softness in U.S. performance seen in the past couple weeks is something we are monitoring. We remain confident that the softness is due to the continuing rebalancing of demand post-pandemic. Weekdays, group demand, and the Top 25 Markets are again driving performance, as was the norm pre-pandemic. The slower return of international travel, especially from China, along with new business travel patterns are likely holding back stronger performance.

Looking ahead

For the U.S., the next three weeks will seem like a boomerang due to the impact of Halloween, which falls on a Tuesday this year. Next week and the week following Halloween are expected to see strong performance as meeting planners along with business and leisure travelers shift travel to these weeks and away from Halloween week. The week of Halloween should see group demand decline significantly as planners understand that families prefer to stay home rather than attend events, along with softness in business travel (generally for the same reason). Globally, performance will continue to show strong gains. We expect lower global growth in 2024 against stronger year-on year-comparisons.

*Analysis by Isaac Collazo, Chris Klauda, Will Anns

About STR

STR provides premium data benchmarking, analytics and marketplace insights for the global hospitality industry. Founded in 1985, STR maintains a presence in 15 countries with a North American headquarters in Hendersonville, Tennessee, an international headquarters in London, and an Asia Pacific headquarters in Singapore. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), a leading provider of online real estate marketplaces, information and analytics in the commercial and residential property markets. For more information, please visit str.com and costargroup.com.