Market Recovery Monitor - 7 May 2022

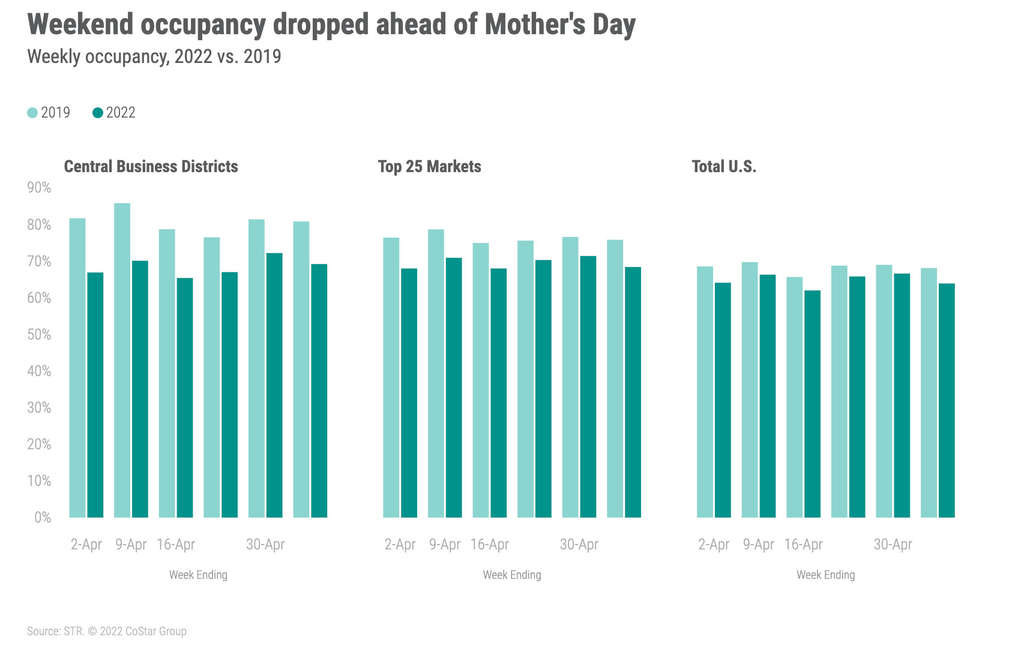

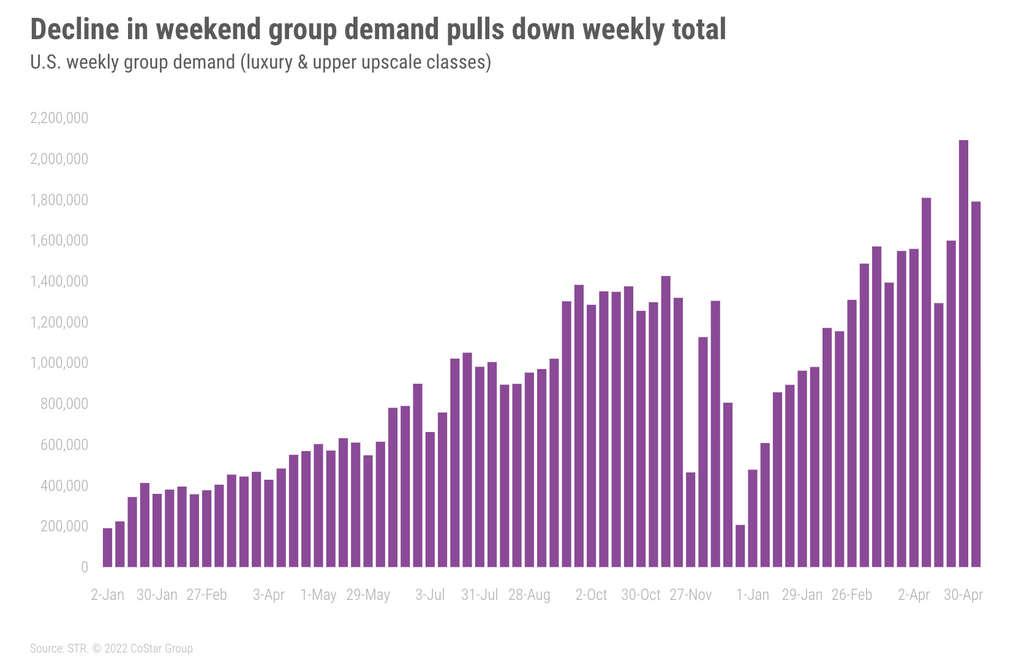

Occupancy dipped in the latest week of reporting, falling 2.7 percentage points week on week to 63.9% during 1-7 May 2022. Travelers opted to stay home for Mother’s Day, and the largest decrease came on the weekend when occupancy fell 5.6 percentage points and accounted for 65% of the weekly demand loss. The impact of the Mother’s Day observance can also be seen in weekend group business, which declined by an amount similar to the Easter weekend (-203K). The news wasn’t all bad, however, as weekday (Monday-Wednesday) occupancy was down only 1.5 percentage points, and several key markets saw their highest occupancy levels of the pandemic-era. Weekly average daily rate (ADR) was basically flat (+0.3%), and revenue per available room (RevPAR) decreased 3.7%.

Comparing with past Mother’s Day weeks, it is normal for occupancy to fall from the preceding week. Further, the week of Mother’s Day has lost occupancy in 16 of the 20 years examined. This year’s Mother’s Day week decrease, however, was the largest since 2004. Reviewing segmentation, the largest share of the demand decline came from the group segment, which accounted for 74% of the room demand lost in the week. The largest loss of groups was on the weekend, when demand dropped by more than 300,000 room nights. The loss of weekend group demand was more than the total decrease in transient demand. In 2019, total group demand, primarily because of less weekend groups, also saw the largest decrease of any segment, but the decline in total demand was mitigated by growth in transient, contract and weekday group business.

While the weekend was down, several markets did well, including Louisville, KY (93.0% occupancy) as the Kentucky Derby led to a 348% week-on-week increase in weekend ADR (US$578), the highest weekend ADR of any market. Strong weekend occupancy (80% or more) was also recorded in Austin, Nashville, Raleigh/Durham, Salt Lake City, San Diego and 13 other markets. Overall U.S. weekend occupancy was 70.8% for the weekend.

Weekday occupancy dropped to 63.3% nationwide with the level settling at 68.5% among the Top 25 Markets, which was the fourth highest of the pandemic-era. Even though weekday occupancy was down across the nation, Boston (72.8%), Minneapolis (63.9%), and Washington D.C. (72.5%) reported their highest levels since the start of the pandemic. Overall, Top 25 Market weekday occupancy ranged from 78.5% in New York to 58.7% in Chicago. NYC’s weekday occupancy was its third highest since the start of the pandemic as the market has recorded five of its six highest occupancies of the pandemic era over the past five weeks.

Central Business Districts (CBDs) also saw occupancy fall with the weekly level dropping to 69.2% from 72.2% in the previous week. Recall, a week prior, CBD occupancy was at its highest value since the start of the pandemic. In this most recent week, occupancy was the third best of the pandemic-era. Room demand for CBDs has been above 90% of the comparable 2019 level for the past three weeks. Weekday occupancy (70.5%) also fell from its pandemic high with the latest week’s level the second highest. CBD weekday ADR (US$229) reached its highest level of the pandemic era with weekday RevPAR (US$162) at its second-best. Among specific CBD submarkets, Boston (81.8%), Denver (83.5%), Minneapolis (82.5%), and Washington D.C. (75.1%) were all at their highest weekday occupancies since the start of the pandemic. Eleven of the 20 CBD submarkets reported weekday occupancy above 70%, which is the same number as in the previous week. Six CBD submarkets saw weekday occupancy reach 80% or more; the largest number since March 2020.

Like the past 12 weeks, ADR remained above the 2019 comparable and was 12% higher than in the comparable week of 2019. The week-on-week change was virtually flat, but excluding the Louisville market, U.S. ADR was down 0.5%. Weekday ADR (+0.3%) declined for a fourth consecutive week but was up among the Top 25 Markets (+1.4%), led by solid-to-strong growth in Boston (+11%), Denver (+10%), Houston (+11%), Minneapolis (+20%), and New York (+9%). CBDs also saw weekday ADR increase (+1.7%) for a third week in a row. Total U.S. weekend ADR was up 1.3%, led again by Louisville and 25 other markets that saw weekend ADR increase by more than 10% week on week. Among the Top 25 Markets, weekend ADR was up 0.7%, driven by Miami, which recorded a 53.9% ADR gain (US$479) via the Miami Grand Prix.

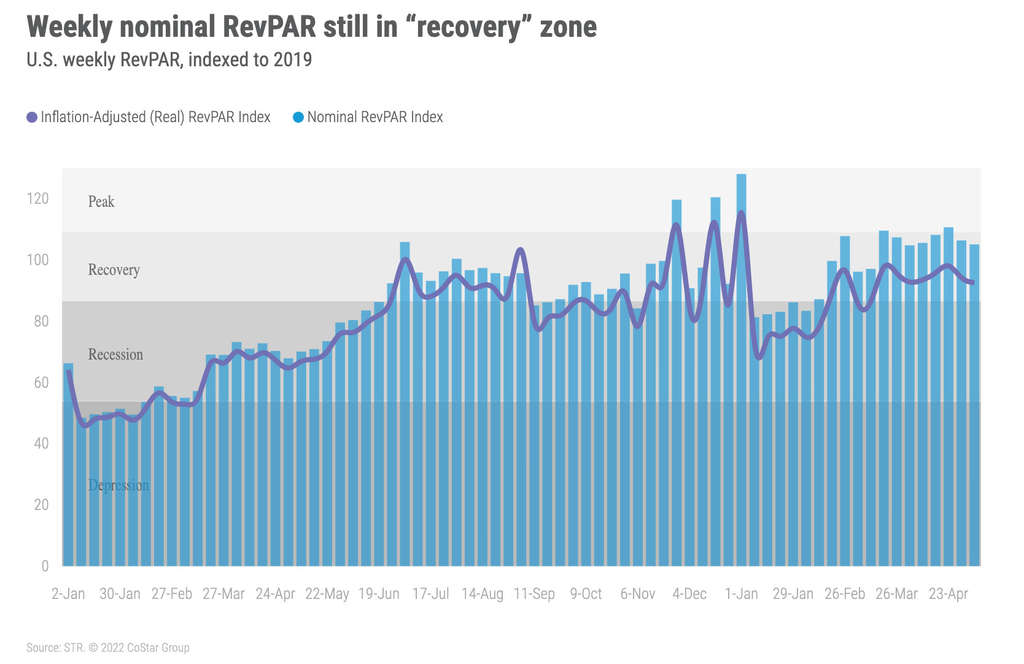

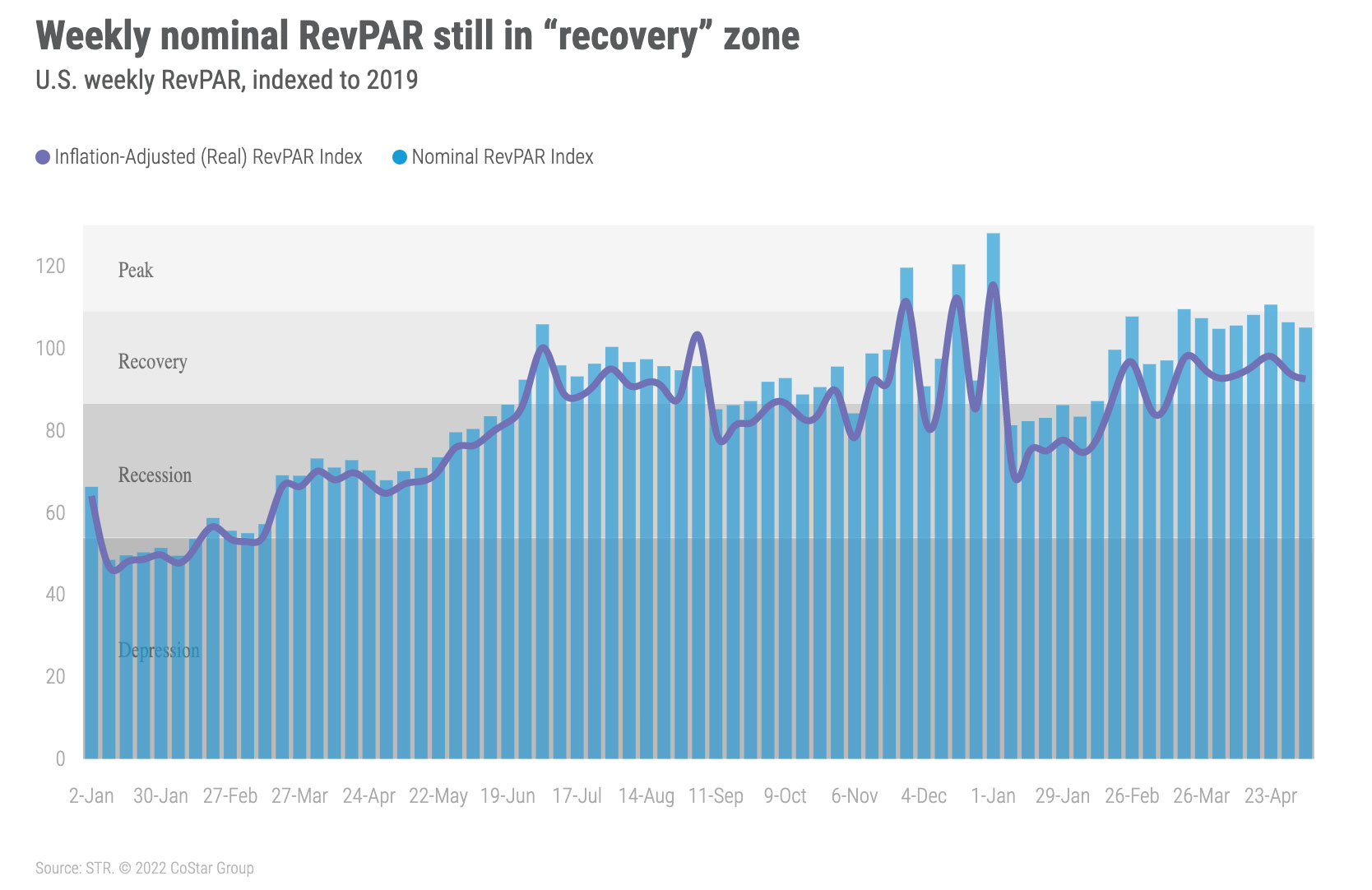

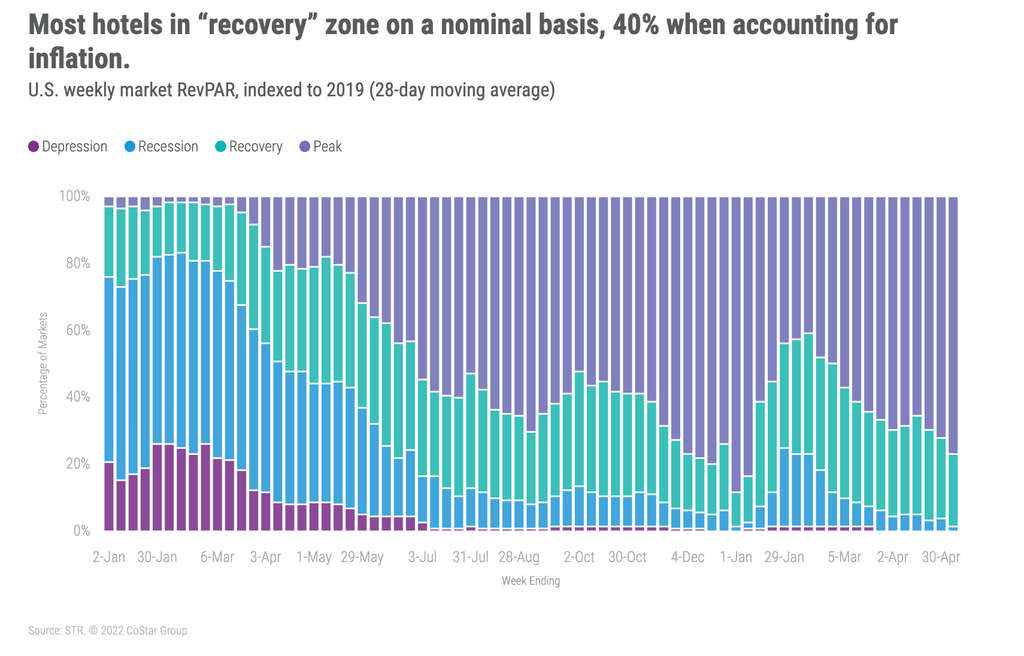

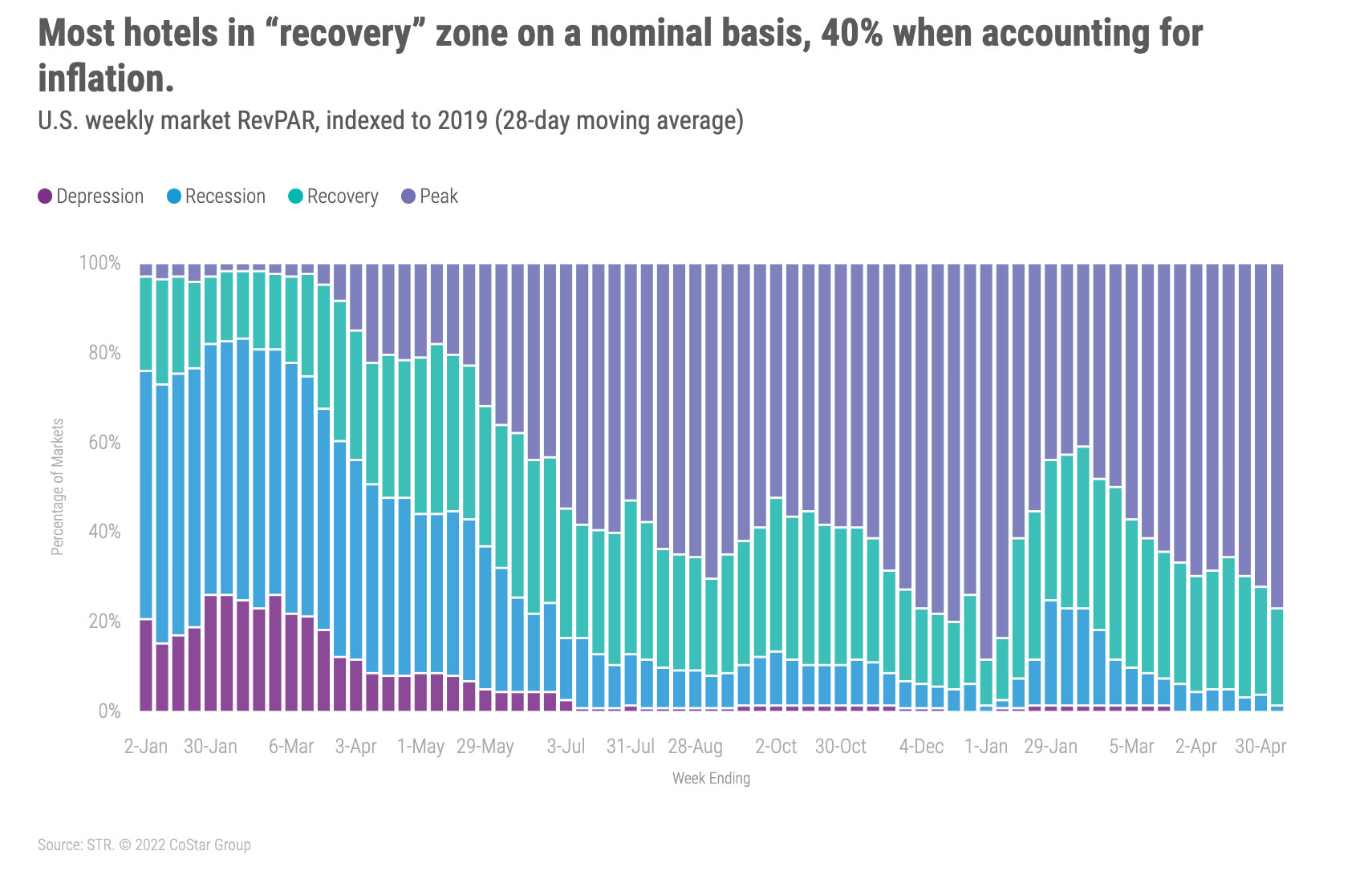

Even though weekly RevPAR declined week over week, it remained ahead of 2019 by 5%. Adjusting for inflation, real RevPAR was 7% lower than in 2019. On a market-level, 115 of the 166 STR-defined markets reported RevPAR higher (“peak”) than what it was in the comparable week of 2019 with another 41 in “recovery” (market RevPAR indexed to 2019 between 80 and 100). Sixty-one markets were at “peak” real RevPAR with 79 in “recovery.” Over the past 28 days, 128 markets were seeing “peak” RevPAR (66 Real RevPAR) as 36 were in “recovery” (82 Real RevPAR).

Around the Globe

Occupancy outside the U.S. increased for a second consecutive week to 57.9%, up 2.3 percentage points. Strong week-on-week occupancy gains were recorded across the Middle East with the end of Ramadan. ADR was also on the rise, up 7.7%, the largest weekly gain since early in the year. RevPAR surged 12.1%.

Among the 10 largest countries based on supply, occupancy (71.5%) was up 1.4 percentage points week on week, led by a strong increase in Indonesia (30 percentage points) and growth in Japan, France, Germany and Italy. Canada, China, Mexico, Spain, and United Kingdom all saw a drop in occupancy.

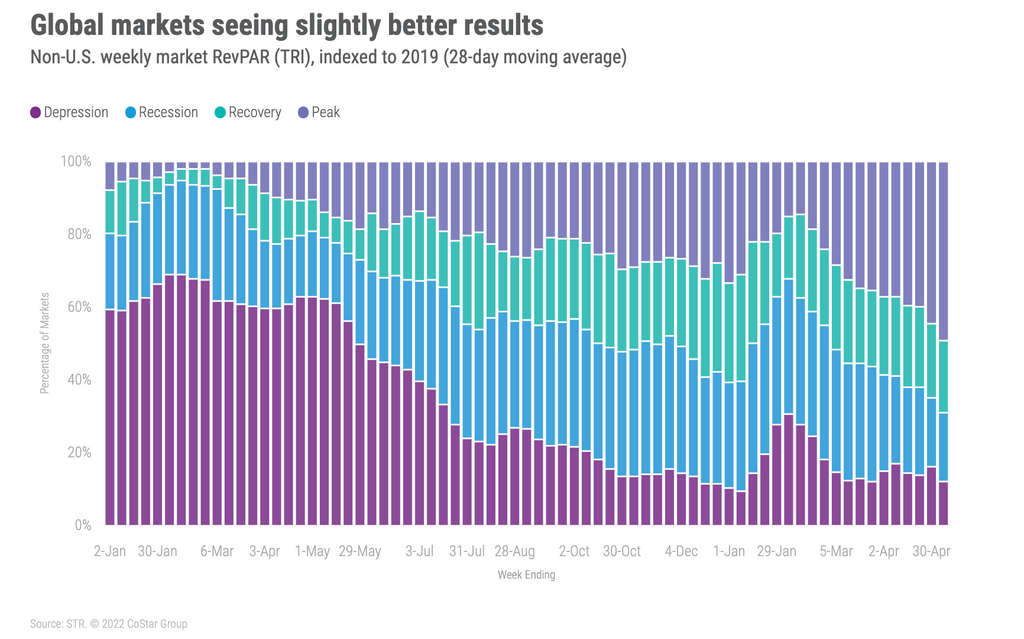

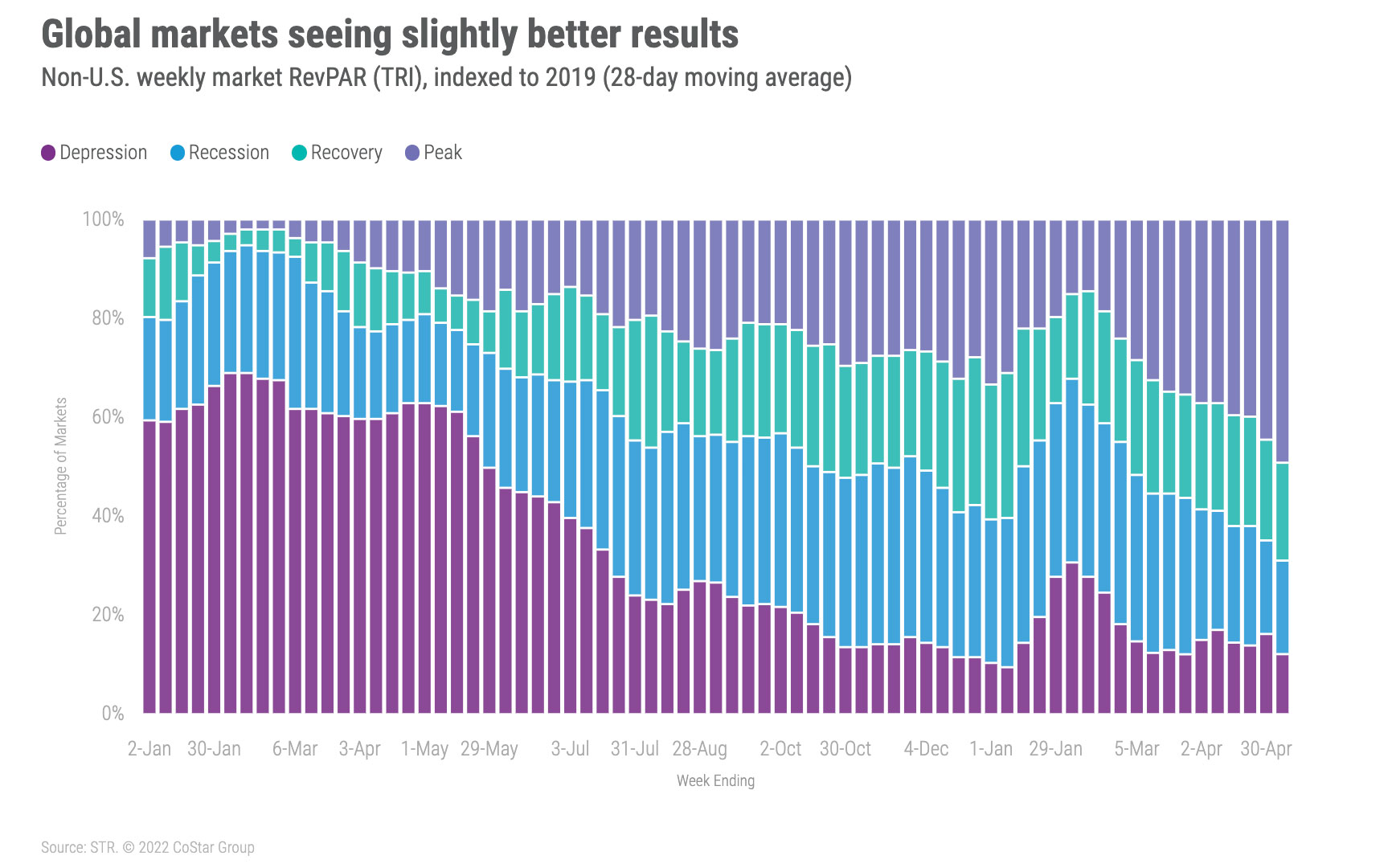

Over the past 28 days, 49% of non-U.S. markets have seen a RevPAR that is higher than what it was in 2019. Twelve percent of markets are in “depression” (RevPAR indexed to 2019 below 50) with 19% in “recession” (RevPAR indexed to 2019 between 50 and 80).

Big Picture

We do not see any red flags regarding the drop in occupancy this week. We remain encouraged by the performance in weekday occupancy, especially among the Top 25 Markets and CBDs. We expect that U.S. demand will pick up in the coming week, supported by a surge in university graduations and increased gains in business and group travel.

In Europe, a noteworthy development can be seen via our Forward STAR data, as most gateway cities are seeing rolling 28-day occupancy into mid-May recover to between 90-100% of 2019 comparables.

Note: After a one-week break, the next edition of the Market Recovery Monitor will be published on Friday, 27 May.

About STR

STR provides premium data benchmarking, analytics and marketplace insights for the global hospitality industry. Founded in 1985, STR maintains a presence in 15 countries with a corporate North American headquarters in Hendersonville, Tennessee, an international headquarters in London, and an Asia Pacific headquarters in Singapore. STR was acquired in October 2019 by CoStar Group, Inc. (NASDAQ: CSGP), the leading provider of commercial real estate information, analytics and online marketplaces. For more information, please visit str.com and costargroup.com.