Is there a direct online channel dilemma?

Background

A recent, very heated, discussion on LinkedIn about direct online vs OTA distribution prompted this article. Some of the direct distribution “detractors” claimed that the direct channel was, quite often, more expensive than the OTA channel, pointing toward ROIs from metasearch marketing, so why bother? Proponents of direct distribution insisted that the direct channel was more than just ROIs that allowed the property to “own” the customer.

Why are we even talking about the direct online channel? Fish where the fish are! Today, the average travel consumer spends almost 7 hours on digital media a day vs 19 minutes on print media (newspapers and magazines). Overall consumers spend more time with digital media than with TV, radio and print media combined (Hootsuite). So, forget about spending your precious marketing dollars on print brochures and collateral, print ads, direct snail mail, etc.

In my view, the question is not about choosing one vs another channel, in this case direct online vs OTA channel, but how to balance your distribution so that your property is the least susceptible to seasonality, group cancellations and calamities, or over dependence on any single distribution channel.

Who “owns” the customer matters!

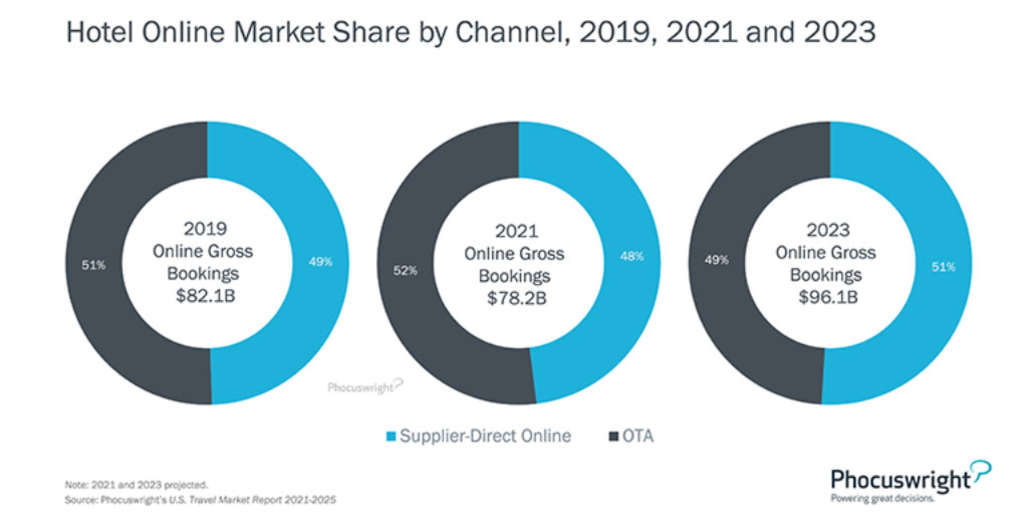

Let’s face it: there have always been intermediaries in hotel distribution, the question is: to what extent? Even in the pre-Internet era, back in 1995, 25% of roomnights were generated by intermediaries vs 75% were direct. In other words, direct vs indirect ratio was 4:1. Fast forward to today: PhocusWright reported that 52% of U.S. gross online hotel bookings in 2021 came from OTAs. In Europe the OTA contribution is even higher, due to the higher market share of independent properties, known to have much higher OTA dependency.

For many independents direct vs indirect (OTAs, bedbanks and other intermediaries) ratio is negative 1:3 and even 1:4. Compare this to major hotel chains’ positive 2.5:1 to 3:1 ratio. Why do the independents have such an over dependence on the OTAs? Systemic underinvestment in talent, technology and digital marketing are the main reasons.

So, is it worth to “own” the customer if you are an independent hotel? Doesn’t customer lifetime value provide benefits only to the major hotel chains?

Outside of the once-in-a-lifetime guests that visit your destination, there are plenty of domestic leisure and business travelers, travelers from neighboring counties, provinces or countries that frequent your destination. These travelers from short- and mid-haul feeder markets are your potential repeat and direct guests, yet very few independents are doing anything to engage, acquire and retain them.

Is the direct channel cheaper than the OTAs?

At NextGuest, now part of Cendyn, we tracked the cost of direct online distribution in the course of 20 years across our more than 5,000 plus primarily independent hotel clients. You know what? The average cost has stayed consistently in the range of 4.25% - 4.5%, including website cost amortized over 36 months, website maintenance, hosting, analytics, digital marketing (Content Marketing, SEO, metasearch, online media, social media, email marketing, CRM marketing, omnichannel marketing campaigns, etc.), consulting fees. Compare this to OTA commissions of 18%-25% plus increased visibility commission add-observations, OTA loyalty member discounts, etc.

The caveat? You have to invest adequately in digital marketing and technology and maintain a very comprehensive, year-round digital strategy, not just embark on occasional, one-off initiatives. Your digital marketing strategy must aim to engage, acquire and retain travel consumers throughout the Digital Customer Journey and its five phases: Dreaming, Planning, Booking, Experiencing and Retention/Sharing.

In my view the cost of acquisition in the direct online channel is only a small part of the equation. “Ownership” of the customer and their first party data, and increasing repeat business are equally important. The hotels “own” their direct online customers - first party data, preferences, pre-, during and post engagements and communications, which enable them to market efficiently in this era of increased privacy regulations, and significantly increase repeat business via CRM and guest appreciation programs, marketing automation, drip campaigns, etc.

Calculating all the benefits above and comparing to the cost of OTA distribution paints a very attractive picture of the direct channel, no doubt about it!

The Direct Channel is the engine that powers repeat business

Repeat guests are 5-15 times cheaper than acquiring new guests, all costs and benefits accounted for. The direct online channel is the engine that generates the property’s repeat business, and repeat business reciprocates by fueling the direct online channel.

Systemic underinvestment by independent hotels in digital marketing, technology and CRM is the reason why less than 10% of roomnights at independents on any given night come from repeat guests (leisure and business combined). Compare this to 58.5% for the major hotel chains and 62% for Marriott and Hilton.

Your past guests already know your property’s location, hotel product and value proposition, and are much cheaper to re-acquire compared to new guests. In the post-pandemic era, success in bringing repeat business will make or break any property. Naturally, you cannot have a meaningful repeat business without investing in digital marketing and technology, including CRM technology and program in place.

CRM not only ensures deep engagement with your past and future guests but allows the property to use your CRM first party data about your best guests to launch similar audiences marketing on Google, Facebook, Instagram, etc. to target potential customers with similar characteristics as your best guests. In addition, CRM initiatives, in combination with ORM (Online Reputation Management) technology, can turn your happy guests into brand ambassadors and avid social media influencers.

CRM technology has become widely available and reasonably priced via hospitality-specialized vendors like Cendyn CRM, Revinate CRM, TravelCLICK GMS, etc., yet less than 10% of independent hotels have implemented CRM programs in place.

Systemic underinvestment = poor direct channel results

How serious is the marketing underinvestment by hoteliers? In “normal” years like 2019, hotels spend on marketing less than 2.5% of net room revenue. STR/CoStar recently released data clearly shows that marketing spending in U.S. hospitality during the pandemic shrank significantly compared to 2019, dropping to as low as 50% in 2020 and rebounding slightly to 54% in 2021 of the pre-pandemic level. In other words, hoteliers spent on marketing 1.35% of net room revenue (54% of 2.5%).

Similar is the situation in technology investments. STR/CoStar data clearly shows that IT spending in U.S. hospitality has declined significantly throughout the pandemic to an average 50% level, compared to before the crisis.

Hoteliers’ marketing and technology spending in Europe and APAC is even worse than in North America.

Check out the related World Panel viewpoint: The Indirect Distribution Dilemma

Check out the related World Panel viewpoint: The Indirect Distribution Dilemma9 experts shared their view

OTA penetration fell drastically during COVID-19 as travelers reached out directly to suppliers to allay safety concerns. But, as we return to the new normal, initial indications are that OTAs are regaining their dominant position within travel distribution. The question is: Is this a certainty, and what can hotels do to retain their newfound market Share?

Viewpoint Sponsored by Shiji Distribution Solutions

Google - your hotel direct channel’s best friend in 2022

Your direct channel starts with your website and Google: This search engine now controls 91.42% global search engine market share (2022, Hootsuite). Google now “owns” the travel consumer and has become the “shepherd of the digital customer journey” by engaging the traveler at each of the five phases of the Digital Customer Journey.

Google has become a fully integrated advertising ecosystem, where all advertising formats are intertwined and work in concert. User engagements in the upper funnel (SEO, content marketing, YouTube TrueView, Gmail Ads, etc.) influences conversions in the lower funnel (Google Business Profile, Google Ads, Google Hotel Ads, Google Display Network, RLSA, Customer Match, etc.), and a campaign in one advertising format directly influences the results from all other formats.

Here are the must-do initiatives on Google for 2022:

- Overhaul your website SEO

- Ensure your property has a mobile-first website and mobile-first content. Make sure the download speed of your website on mobile devices is below 2.5 seconds to avoid your site being penalized by Google and reduce its bounce and abandonment rates.

- Install automated schema markup on your property website, which helps search engines understand the content and intent of your site, especially dynamic content elements such as events and happenings pages, special offers, opening hours, and star ratings.

- Invest in content marketing, which elevates your hotel website importance in the eyes of Google via the inbound links and citations it creates.

- Update your Google Business Profile (GBP): Make sure your GBP is fully optimized with your property information, amenity and services descriptions, business hours, your COVID cleanliness programs, hotel images and videos, etc.

- Google Reviews: Google now has more hotel customer reviews than all of the review and OTA websites combined! Make sure you respond daily to the reviews via the management dashboard on GBP.

- Join Google Hotel Ads (GHA): both free and paid PPS (Pay Per Stay) listings

- Launch Google Ads (GA): Launch hotel-branded keyword terms campaign to target past guests in the short-haul and drive-in feeder markets

- Google Display Network (GDN): Launch a GDN Retargeting campaign, targeting users who have visited your website and are already familiar with your product, offerings and location.

Should metasearch be considered a direct channel?

Metasearch has not been a direct online channel for some time now, at least since Google introduced their PPS model (Pay per Stay) model where hotels pay a commission only if the guest actually stays at the property. Trivago recently adopted a similar model. All these metasearch channels: Google HPA, Tripadvisor Metasearch, Trivago, Kayak Hotels, etc. have become pure commission-based distribution channels, same as Booking.com, Expedia, etc. API connectivity is done in most cases by the CRS, channel managers or cloud PMS. Many hotels have already transferred responsibility for these channels to the revenue management team, in charge of third-party distribution.

Conclusion

So, is there a direct online channel dilemma? No, there isn’t! It is of utmost importance to balance your distribution portfolio and the direct online channel plays a crucial role in this strategy. If you invest adequately in digital marketing and technology, including CRM, and improve your property’s website, you can significantly increase revenues from the direct online channel and repeat business. In this way you can balance your distribution, decrease your OTA dependency, and add hundreds of thousands of dollars to the bottom line, making your property less susceptible to seasonality, group cancellations and calamities, or over dependence on any single distribution channel.